[ad_1]

West Facet Capital finds resilience amid monetary stress | Australian Dealer Information

Information

West Facet Capital finds resilience amid monetary stress

Folks spending much less to to allow them to pay mortgage

Australian debtors in Western Sydney have “rallied across the residence” and targeted on paying their mortgage throughout occasions of price rises and monetary stress, in accordance with West Facet Capital managing director Tony Nguyen.

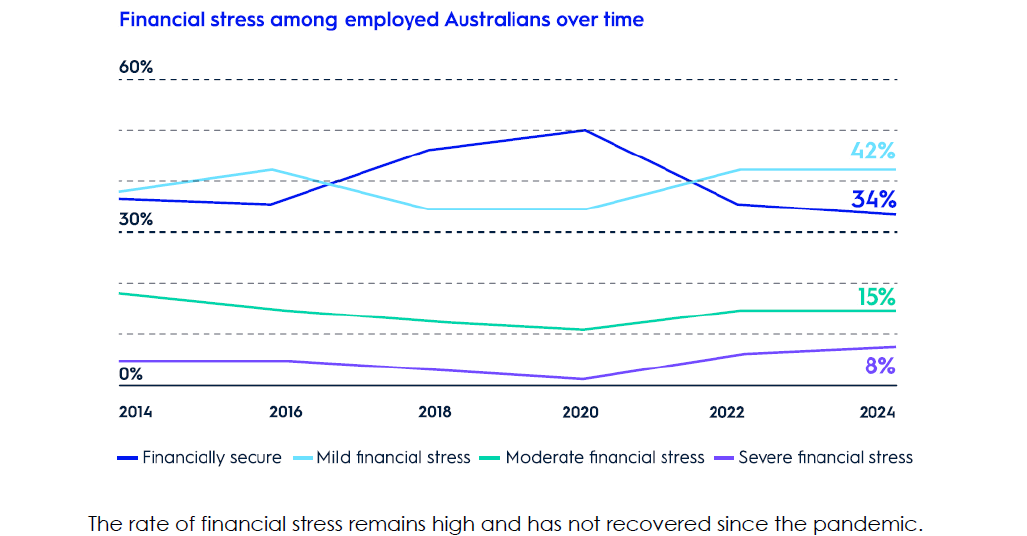

AMP’s Monetary Wellness report, which surveyed 2,475 Australians aged 18 and over in July2 2024, discovered monetary stress ranges in Australia are actually at their highest level in 10 years, with only one in three at the moment feeling financially safe.

Nguyen (pictured above left), who providers primarily PAYG wage incomes purchasers and SME enterprise house owners dwelling in Western Sydney, mentioned he had seen proof of stress as rates of interest rose.

“We did obtain much more calls because the rates of interest began going up and folks have been in a panic and whatnot, understanding what they’ll do and what their choices have been, that type of stuff,” Nguyen mentioned. “So [financial] stress from that standpoint was obvious.”

Nevertheless, he mentioned what he had seen greater than something was that his purchasers, and Australians usually, have been fairly resilient, and that in distinction to “doomsday eventualities” most had simply been spending much less.

“They did precisely what the RBA meant. They spent much less as a complete.”

Nguyen mentioned that, as a lot of his purchasers have been good savers, they have been additionally capable of faucet into financial savings. Whereas these had been depleted, it had allowed them to climate the rate of interest hikes.

“Everybody simply rallied across the residence, they needed to guard their residence, they usually simply spent much less elsewhere.”

Australians are responding to the powerful monetary setting by spending much less – the report discovered one in three Australians had cancelled streaming subscriptions and gymnasium memberships.

AMP Financial institution group government Sean O’Malley (pictured above proper) mentioned the monetary insecurity uncovered by the report was not stunning given value of dwelling pressures and housing unaffordability challenges being confronted.

“And whereas the analysis tells us that almost all are assembly their mortgage repayments, we all know that financial savings charges are down and lots of are slicing again expenditure on family fundamentals akin to groceries, and different extra discretionary objects akin to streaming providers and holidays,” O’Malley mentioned.

Supply: AMP Monetary Wellness Index, July 2024

When it got here to residence loans, debtors had targeted on assembly their repayments.

“It’s an adage, isn’t it, that it at all times appears onerous till you do it,” Nguyen mentioned.

“There was a little bit of panic, when folks have been saying, ‘How can I afford it?’. Nicely, guess what? They did afford it. In relation to their residence, you don’t promote your private home simply because the charges go up, you might be considering of different methods to maintain your private home.”

AMP discovered stress ranges have been additionally rising for these incomes between $100,000 and $500,000, with one in 4 on this revenue bracket both ‘severely’ or ‘reasonably’ financially harassed.

Nguyen steered a few of these debtors could have been seduced by “life-style inflation”.

“Managing cash is an artwork kind. Some folks have it. Some folks do not. Simply because you may have extra of the revenue doesn’t suggest you are a greater cash supervisor,” he mentioned.

Function for brokers to coach purchasers

AMP discovered many individuals have been specializing in short-term monetary calls for reasonably than long-term planning, with one in three Australians saying they by no means or hardly ever deliberate for his or her monetary future.

One in three Australians are additionally nonetheless not utilizing any data sources in any respect to tell necessary monetary choices, even simply accessible data akin to podcasts, social media, or Google.

This might present a chance for finance brokers to help consumer schooling, although Nguyen mentioned that his strategy to consumer service was at all times the identical, whether or not charges have been going up or down.

“You at all times must be able the place you interact with us and we may help evaluation your charges regularly. As a result of we do this, the message has at all times been the identical,” he mentioned.

Associated Tales

Sustain with the most recent information and occasions

Be a part of our mailing checklist, it’s free!

[ad_2]

Source link

")

{kind=link}