[ad_1]

Present funds, which can be utilized for down funds and shutting prices, might be a good way to minimize the burden of shopping for a house as a veteran.

This information supplies a complete overview of those subjects, making certain veterans have the knowledge to make knowledgeable selections about their dwelling buy and financing choices.

What’s a Present Fund?

A present fund is a financial reward supplied by members of the family, buddies, or different benefactors to help with the acquisition of a house.

These funds are significantly precious in VA loans since they can be utilized for closing prices, down funds, or different mortgage-related bills with out the expectation of reimbursement.

By lowering the burden on veteran homebuyers, homeownership turns into extra inexpensive and accessible.

The reward fund differs from a mortgage as a result of it doesn’t require reimbursement; the giver doesn’t anticipate any return or compensation for the reward.

The approval and phrases of VA loans rely on making certain that reward funds are literally items. To make the most of these funds successfully, veterans should adhere to VA pointers and preserve correct documentation.

Eligibility of Present Donors for VA Loans

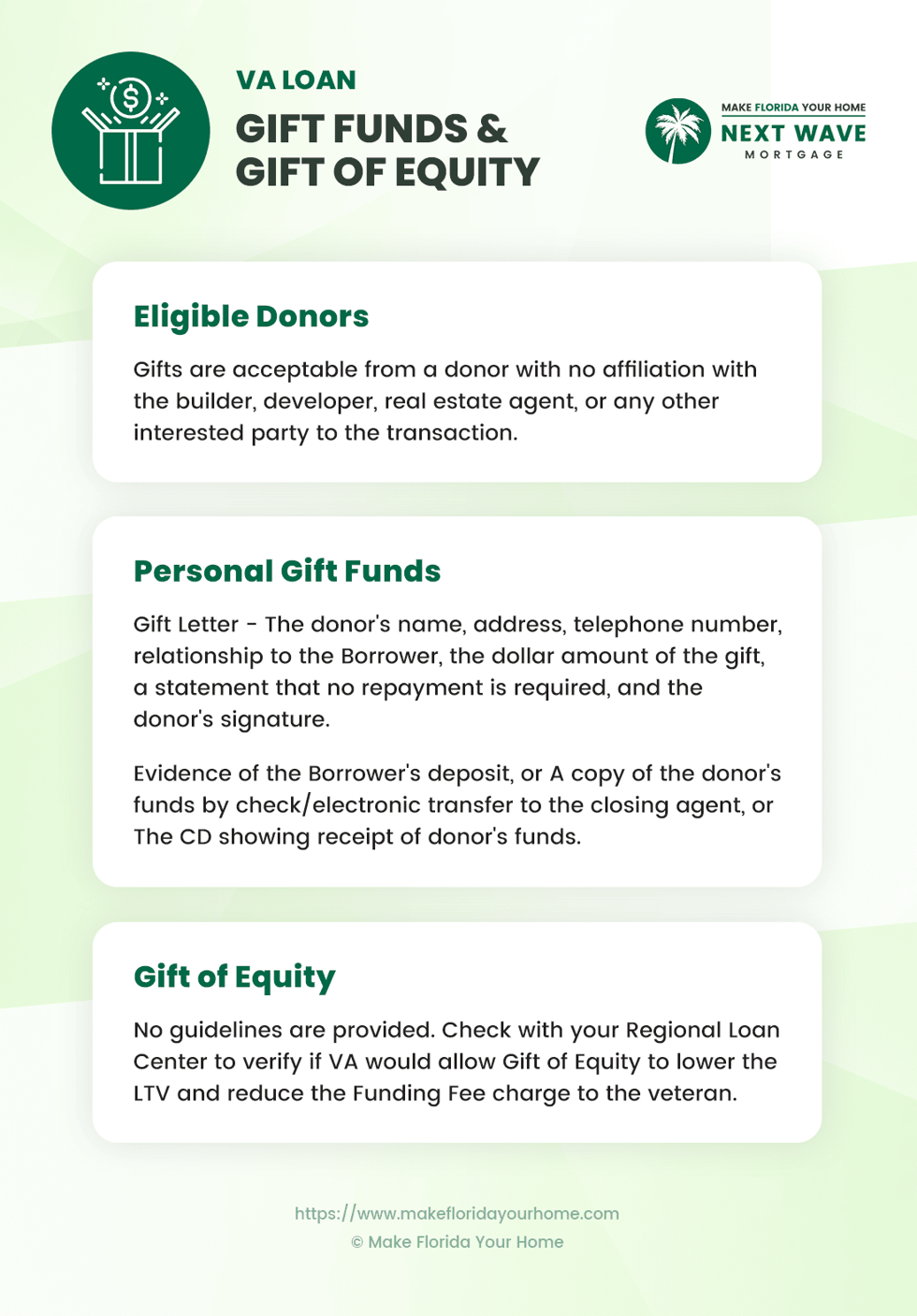

In keeping with the VA Lenders Handbook, Chapter 4, 4-d, an eligible reward donor is outlined as any particular person who doesn’t have an affiliation with the builder, developer, actual property agent, or every other get together to the transaction.

Because of this definition, members of the family, buddies, and different beneficiant contributors will be capable to contribute to the veteran’s dwelling buy with out having any involvement within the sale.

By requiring a real gesture, the VA ensures that the reward isn’t getting used to affect the transaction or to demand reimbursement.

“Items are acceptable from a donor with no affiliation with the builder, developer, actual property agent, or every other get together to the transaction,” as outlined within the Handbook.

This rule is designed to keep up the VA mortgage program’s integrity and shield the veteran homebuyer’s pursuits.

To stop potential conflicts of curiosity or unethical preparations which may drawback veterans, the VA requires that donors haven’t any direct monetary or private curiosity within the sale.

Thus, the reward is concentrated solely on helping the veteran in changing into a home-owner, reinforcing the dedication of the VA mortgage program to serve returning veterans.

Acceptable Present Sources and Makes use of for VA Loans

Acceptable reward sources for VA loans usually are not explicitly restricted by the U.S. Division of Veterans Affairs so long as the donor doesn’t have an affiliation with the builder, developer, actual property agent, or every other get together within the transaction.

Nonetheless, widespread sources of reward funds which can be usually accepted embody:

Household Members: Dad and mom, siblings, grandparents, youngsters, aunts, and uncles can present reward funds. Prolonged members of the family might also be thought of acceptable donors.

Fiancés or Home Companions: People with a longstanding relationship with the borrower that may be simply documented.

Shut Associates: Associates who’ve a clearly outlined and documented relationship with the borrower, indicating a major private connection that would logically assist the reward.

Employers or Labor Unions: Organizations or entities the borrower is related to, corresponding to their place of employment or a labor union member.

Charitable Organizations: Non-profit organizations or group teams that help veterans or homebuyers.

Authorities Businesses or Public Entities: Applications supply veterans or first-time homebuyers homeownership help.

Below VA mortgage pointers, a suitable reward is a voluntary switch of funds from the donor to the veteran borrower, with no expectation of reimbursement.

These items function an important useful resource for veterans, aiding them in masking the monetary necessities of buying a house.

The VA’s method to reward funds is designed to make sure these contributions are real items, thus supporting veterans of their path to homeownership.

Items below VA mortgage pointers can be utilized for varied functions, making them a flexible instrument for veterans’ home-buying course of.

Particularly, acceptable items embody:

Down Fee Help: Items can be utilized to make the down cost on a house, making it simpler for veterans to safe financing while not having private financial savings.

Closing Prices: Items can cowl closing prices, that are varied charges for finalizing the mortgage. This may embody appraisal charges, title insurance coverage, and extra.

Paying Off Money owed: In some circumstances, items can be utilized to repay money owed to enhance the veteran’s debt-to-income ratio, a key consider mortgage qualification.

Prepaids: These are upfront prices paid at closing, together with house owner’s insurance coverage, property taxes, and preliminary escrow deposits.

The pliability of utilizing items for these bills permits veterans to leverage the generosity of their community, thereby lowering the monetary burden of buying a house.

This adaptability highlights the VA mortgage program’s dedication to offering veterans with accessible pathways to homeownership, emphasizing this system’s objective to honor those that have served by making the dream of proudly owning a house extra attainable.

Pointers for Private Present Funds

The VA Lenders Handbook supplies a foundational overview of reward funding acceptance inside the VA mortgage course of.

Nonetheless, it doesn’t delve into intensive extra steering relating to private reward funds. Private items ought to adhere to some easy however essential necessities as a result of absence of detailed directives.

All events concerned are protected by these situations to make sure that reward funds are certainly real items and usually are not anticipated to be repaid, sustaining the integrity of the mortgage course of.

Donor Eligibility: Items have to be from people with out affiliation to the transaction, together with builders, builders, actual property brokers, or every other events.

Present Letter: A letter from the donor is required, together with their title, deal with, phone quantity, relationship to the borrower, the reward quantity, an announcement that no reimbursement is anticipated, and the donor’s signature.

Proof of Switch: Documentation displaying funds switch from the donor to the borrower or closing agent, corresponding to a financial institution assertion or transaction receipt, is important.

No Reimbursement: It have to be clear that the reward isn’t a mortgage and that no reimbursement is anticipated or required.

The essential necessities for private items are vital for donors and recipients to grasp. The VA emphasizes that reward funds have to be sourced from people with out affiliation to the actual property transaction, excluding builders, builders, actual property brokers, or any associated events.

This guideline is designed to stop conflicts of curiosity and make sure the reward’s authenticity, supporting the veteran borrower’s monetary wants with out compromising the transaction’s impartiality.

Documentation for Private Present Funds

Particular documentation is required to simply accept and make the most of private reward funds inside the VA mortgage course of. This documentation verifies the reward’s legitimacy and the donor’s intentions, aligning with VA pointers.

The required paperwork embody:

Present Letter Necessities

A complete reward letter should accompany any private reward funds. This letter must include a number of key items of data to satisfy VA requirements:

Donor’s Title, Deal with, and Phone Quantity: These particulars assist establish the donor and supply contact data for verification functions.

Relationship to the Borrower: Clarifying the connection ensures that the donor has no prohibited curiosity in the actual property transaction.

Greenback Quantity of the Present: Specifies the quantity given to the borrower.

Assertion of No Reimbursement Required: This declaration is essential, because it confirms the reward doesn’t must be repaid, distinguishing it from a mortgage.

Donor’s Signature: The signature verifies the donor’s acknowledgment and settlement to the phrases outlined within the reward letter.

Proof of the Borrower’s Deposit

Along with the reward letter, proof of the reward’s switch and receipt is required:

This documentation is important for correctly dealing with private reward funds inside the VA mortgage framework. It ensures transparency, compliance, and the graceful development of the mortgage utility course of, in the end aiding veterans in securing financing for his or her dwelling purchases.

What’s A Present of Fairness, and How Can They Assist Veterans?

A present of fairness includes the sale of a property beneath its market worth, the place the distinction between the sale worth and the market worth is taken into account a present of fairness from the vendor to the client. This idea is especially related in VA loans when a member of the family sells the property to a veteran.

The fairness, or the property’s worth not lined by the mortgage, successfully contributes to the veteran’s dwelling fairness. This may considerably cut back the Mortgage-to-Worth (LTV) ratio, which is the comparability between the quantity of the mortgage and the worth of the house.

A decrease LTV ratio can profit the borrower by probably lowering the VA funding payment, a one-time payment paid to the Division of Veterans Affairs to assist assist the mortgage program.

Regardless of the potential advantages of a present of fairness, corresponding to lowering the amount of money a purchaser wants at closing and probably reducing the funding payment, the VA Lenders Handbook doesn’t present particular pointers on items of fairness.

The absence of detailed directions implies that accepting and utilizing a present of fairness can rely on varied elements, together with lender insurance policies and the interpretation of VA mortgage necessities.

Given this lack of steering from the VA, it is vital for veterans serious about utilizing a present of fairness to seek the advice of with MakeFloridaYourHome or one other trusted lender.

We will supply personalised recommendation and make clear whether or not a present of fairness is allowable in your state of affairs. We will additionally present data on required documentation and any extra steps to incorporate a present of fairness as a part of a VA mortgage transaction.

In abstract, whereas a present of fairness can supply substantial monetary advantages to veterans buying a house from a member of the family, navigating the method requires a cautious method.

By reaching out to MakeFloridaYourHome, veterans can guarantee they meet all necessities and maximize the benefits obtainable by way of the VA mortgage program.

Steadily Requested Questions About Present Funds for VA Loans

Who can present reward funds in accordance with VA mortgage pointers?

Items for VA loans might be supplied by anybody who doesn’t have an affiliation with the builder, developer, actual property agent, or every other get together within the transaction. This ensures the integrity of the reward, confirming the sale of the property doesn’t affect it.

What can reward funds be used for in a VA mortgage?

A VA mortgage can use reward funds for down cost, closing prices, or different loan-related bills. This flexibility helps veterans and navy personnel handle buying a house’s funds.

Is there a restrict to the quantity of reward funds one can obtain?

The VA doesn’t restrict the reward funds a borrower can obtain. Nonetheless, lenders could have their very own pointers, so it is important to seek the advice of together with your lender.

Do reward funds must be repaid?

No, reward funds don’t must be repaid. The donor should present a present letter stating that the funds are a present and no reimbursement is anticipated.

What documentation is required for reward funds in a VA mortgage?

For reward funds, the borrower should present a present letter from the donor that features the donor’s title, deal with, phone quantity, relationship to the borrower, the quantity of the reward, an announcement that no reimbursement is required, and the donor’s signature.

Can reward funds be used for your complete down cost on a VA mortgage?

Sure, reward funds can cowl your complete down cost, supplied the funds meet VA and lender pointers and are correctly documented.

What occurs if the donor of the reward funds is affiliated with the actual property transaction?

Items from donors affiliated with the actual property transaction (e.g., builder, developer, actual property agent) are unacceptable below VA pointers to stop conflicts of curiosity.

How do reward funds have an effect on the loan-to-value (LTV) ratio?

Present funds used in the direction of the down cost can decrease the loan-to-value ratio, probably enhancing mortgage phrases and lowering the funding payment.

Can a member of the family present reward funds?

Sure, members of the family can present reward funds for a VA mortgage so long as they don’t have any affiliation with the actual property transaction.

Are there any particular pointers for items of fairness in VA loans?

The VA Lenders Handbook doesn’t present particular pointers for items of fairness. Debtors are suggested to test with their Regional Mortgage Middle for eligibility and documentation necessities relating to items of fairness.

Backside Line

Using reward funds inside the VA mortgage course of presents veterans and lively navy personnel a major benefit in reaching homeownership.

These funds, which may cowl down funds, closing prices, and different loan-related bills, present monetary flexibility and assist. The hot button is making certain that reward funds come from eligible donors and are correctly documented in accordance with VA pointers.

By leveraging reward funds correctly, veterans can navigate the home-buying course of extra successfully, making the dream of proudly owning a house extra accessible and inexpensive.

[ad_2]

Source link

")

{kind=link}