[ad_1]

pagadesign

Like practically all different developed nations, the US is dealing with a extreme debt downside.

Right now, public debt is almost $35 trillion, rising roughly 23% within the final 4 years alone.

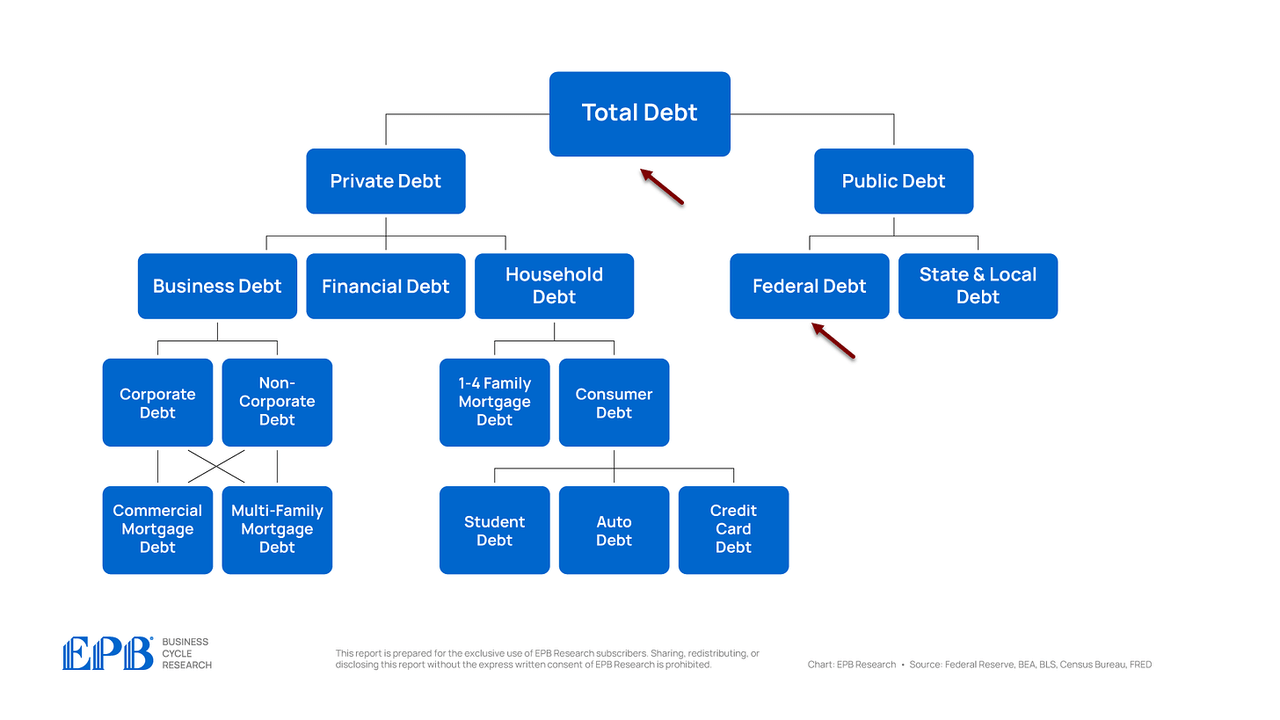

However public debt solely tells one half of the whole story: what the federal government owes.

The US additionally has $66 trillion of personal debt – what firms and households owe.

So, on this article, we’ll not solely break aside the debt state of affairs within the public sector, however we’ll additionally analyze the non-public sector debt burden. On the finish of this text, we’ll talk about the results of such a crushing private and non-private debt burden.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

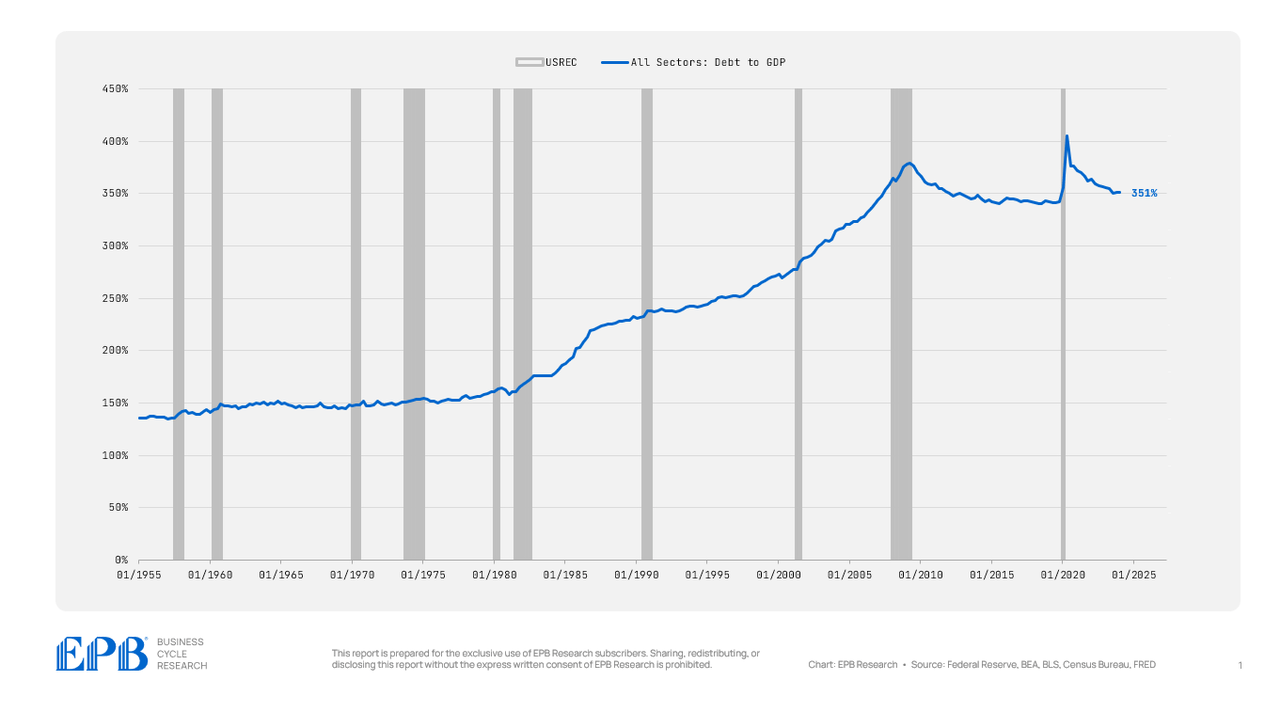

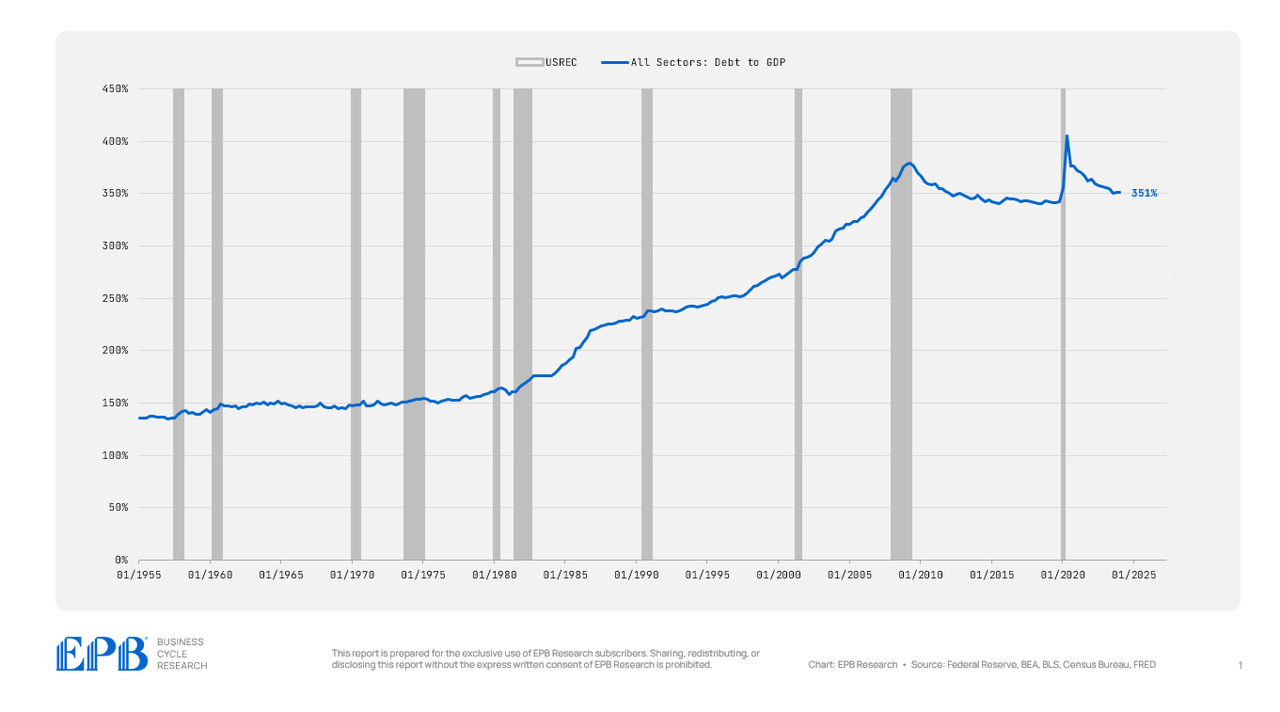

From 1955 by 1980, complete debt averaged 150% of GDP, however that has greater than doubled during the last 40 years.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

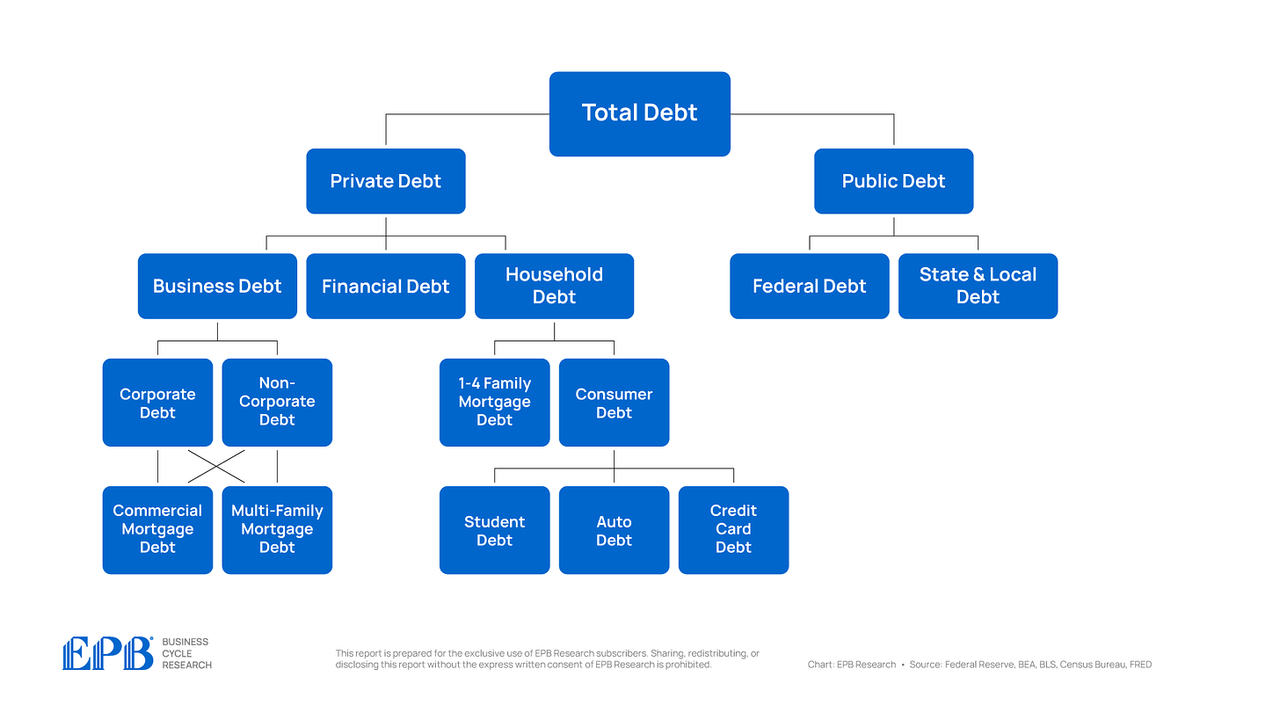

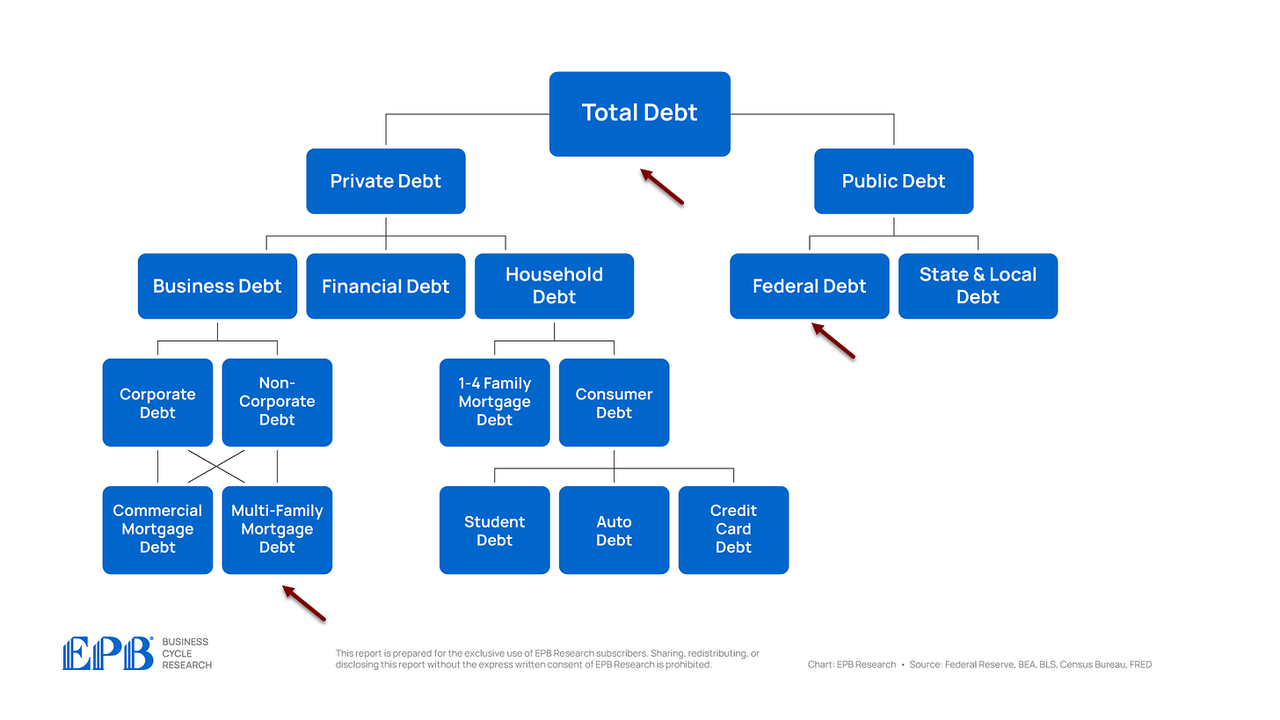

For all sectors of the financial system, we’re going to have a look at the debt ranges at present, the debt ranges in 2007 earlier than the final main debt disaster, and the typical debt stage from 2012 to 2019 to get an concept of whether or not the financial system or a selected sector is at important threat.

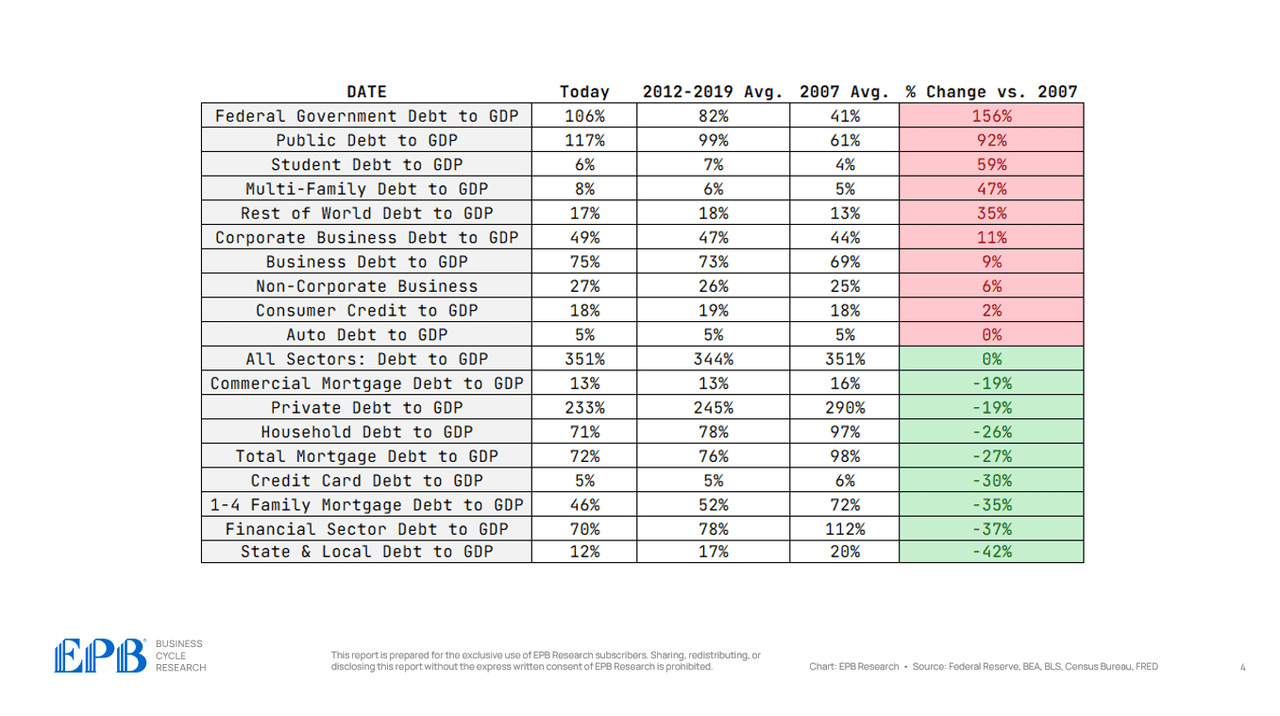

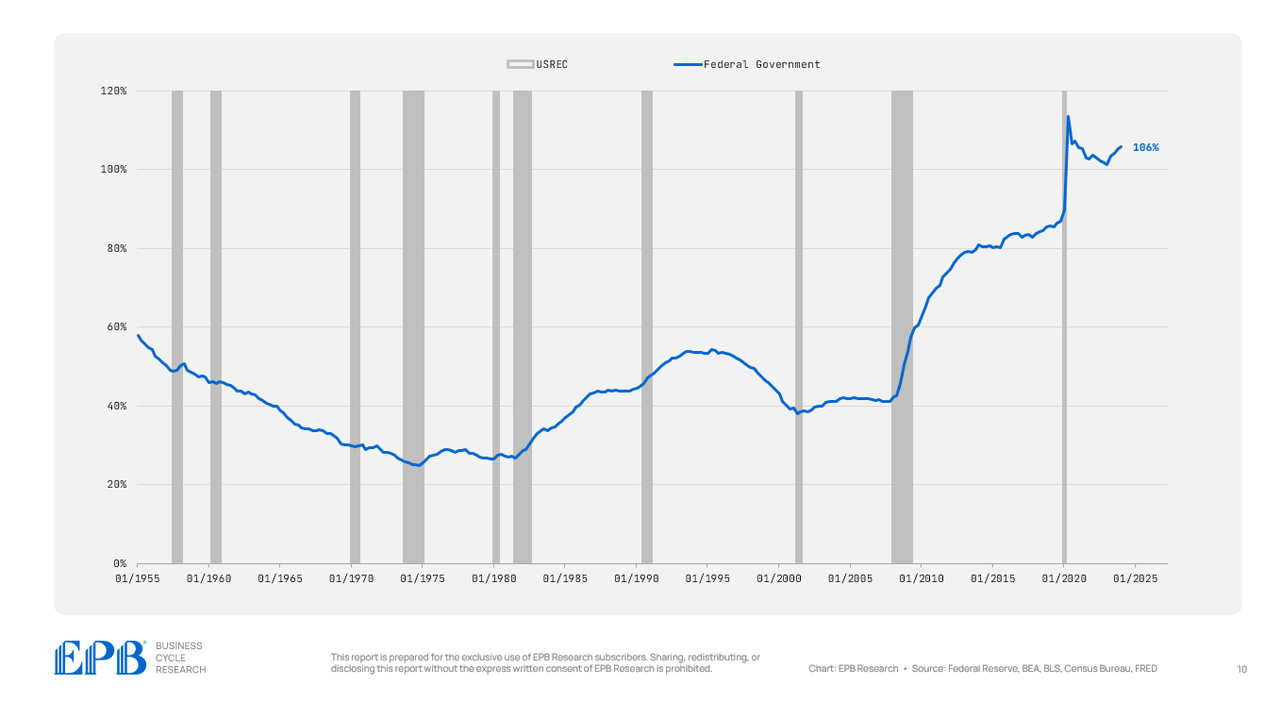

For instance, if we have a look at the primary line within the chart beneath, we are able to see that federal authorities debt is 106% of GDP at present. It averaged 82% from 2012 by 2019 and 41% in 2007. In comparison with 2007, debt to GDP has elevated 156%, a large enhance within the federal authorities’s debt burden.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

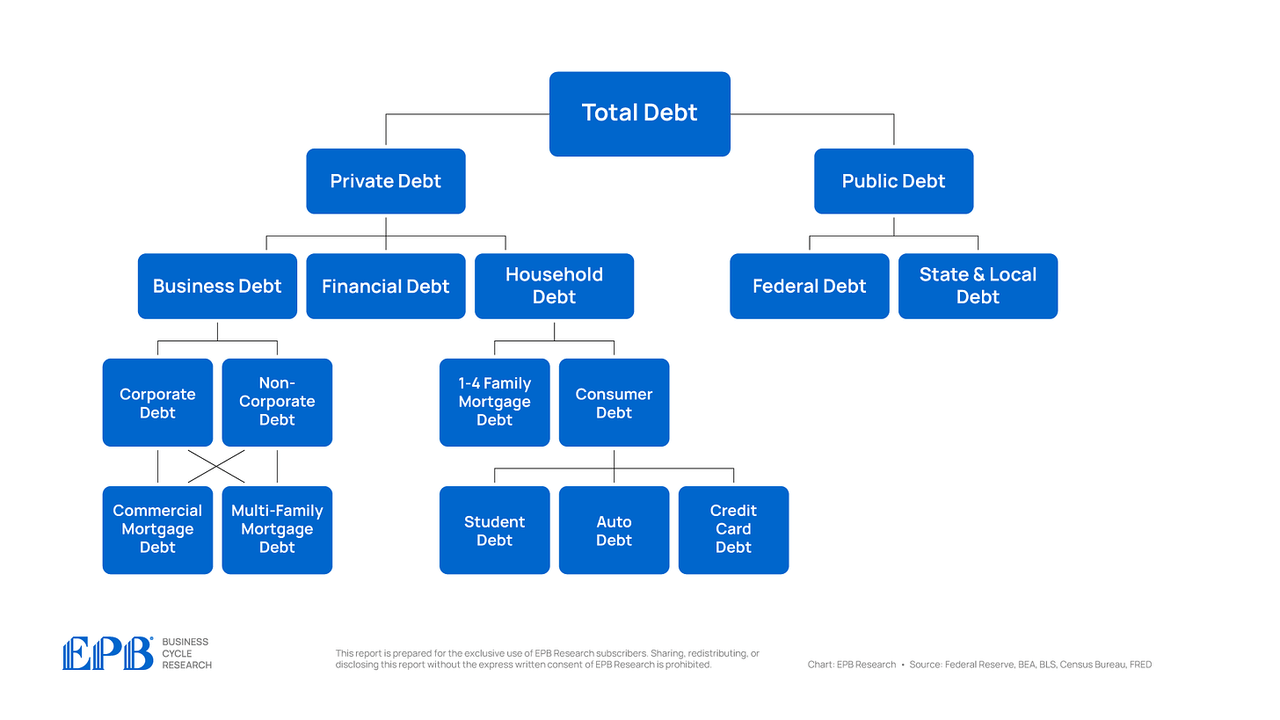

We are going to undergo a course of like this for every layer of debt to uncover the most important points dealing with the US financial system at present.

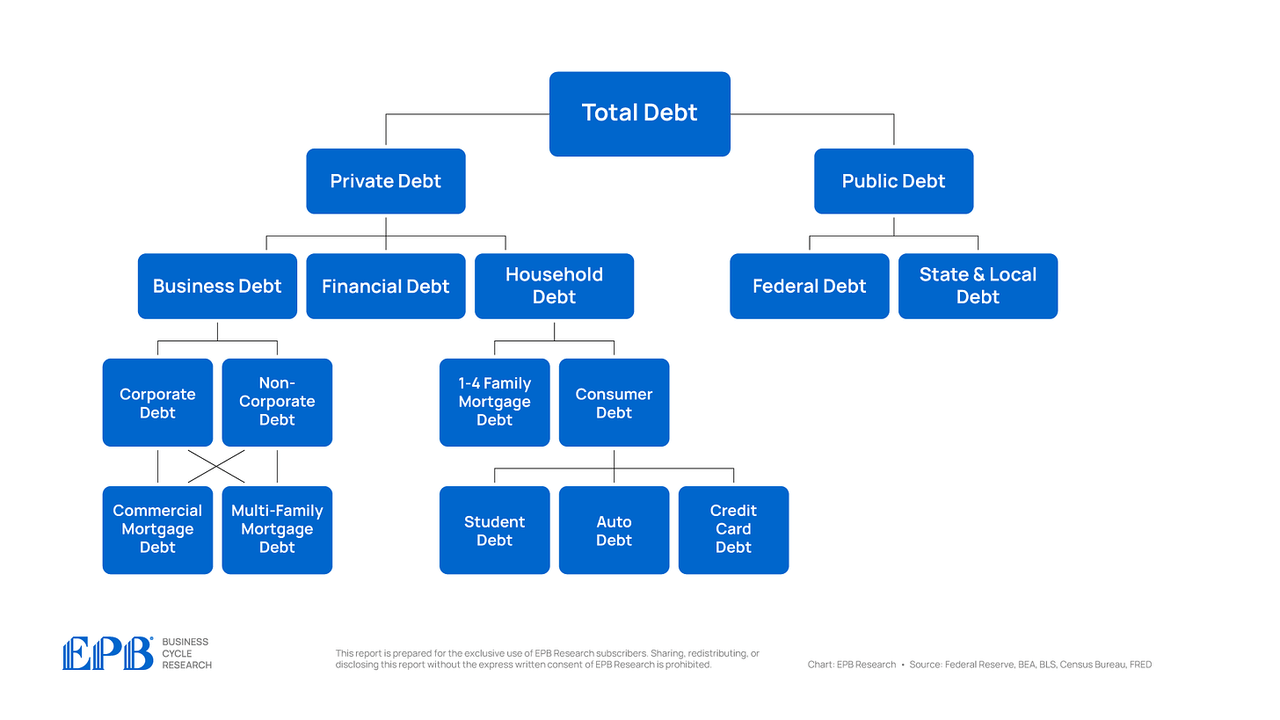

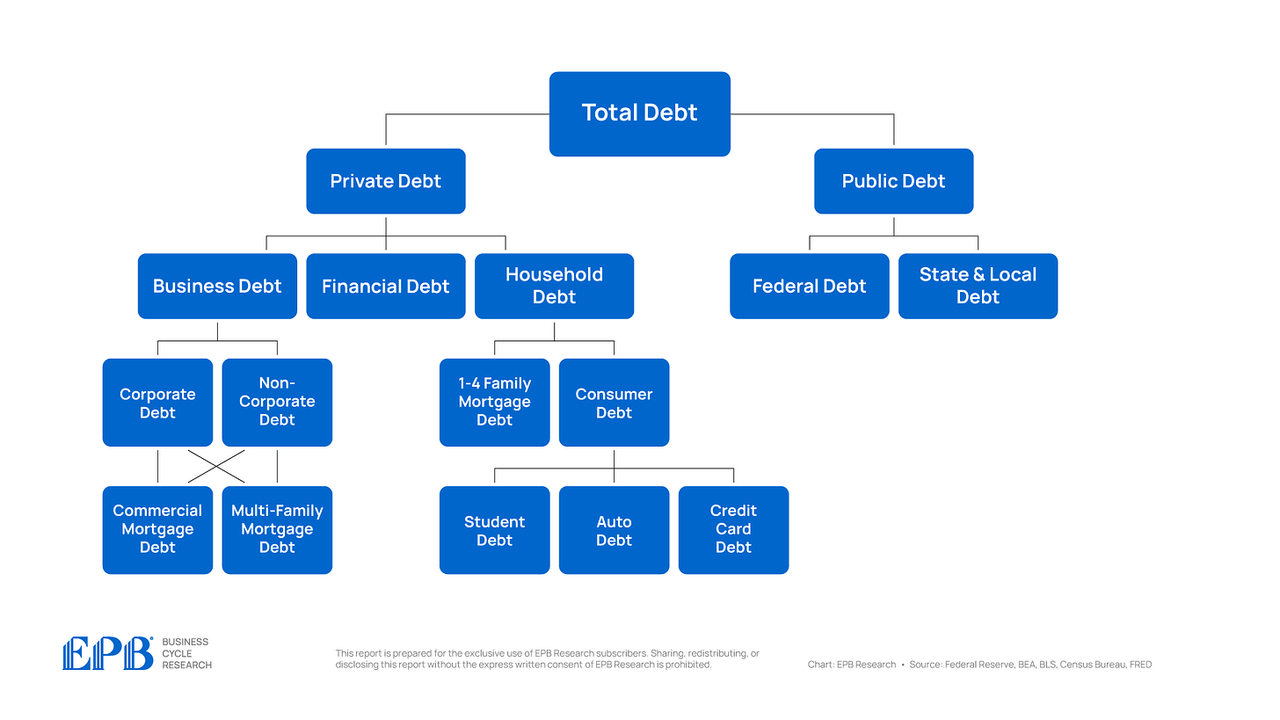

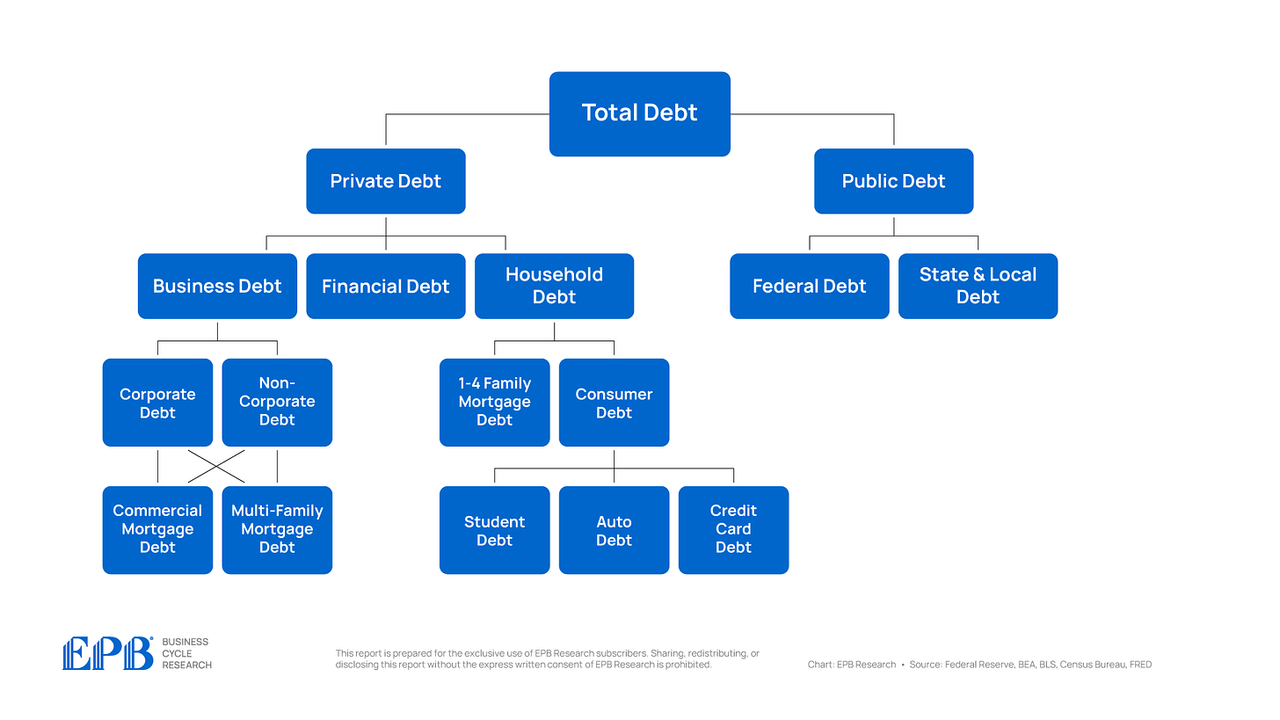

Let’s begin by taking a look at complete debt to GDP, which incorporates all sectors of the financial system, each the non-public sector and the federal government sector.

The financial system has a complete debt to GDP ratio of 351%. This compares to a median of 344% from 2012 to 2019 and 351% in 2007. So the financial system, as an entire, has not deleveraged in any respect from the 2007 disaster and the years that adopted.

There’s a large build-up of debt that’s crushing the typical American, resulting in weaker financial prospects as there was no internet discount in debt.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

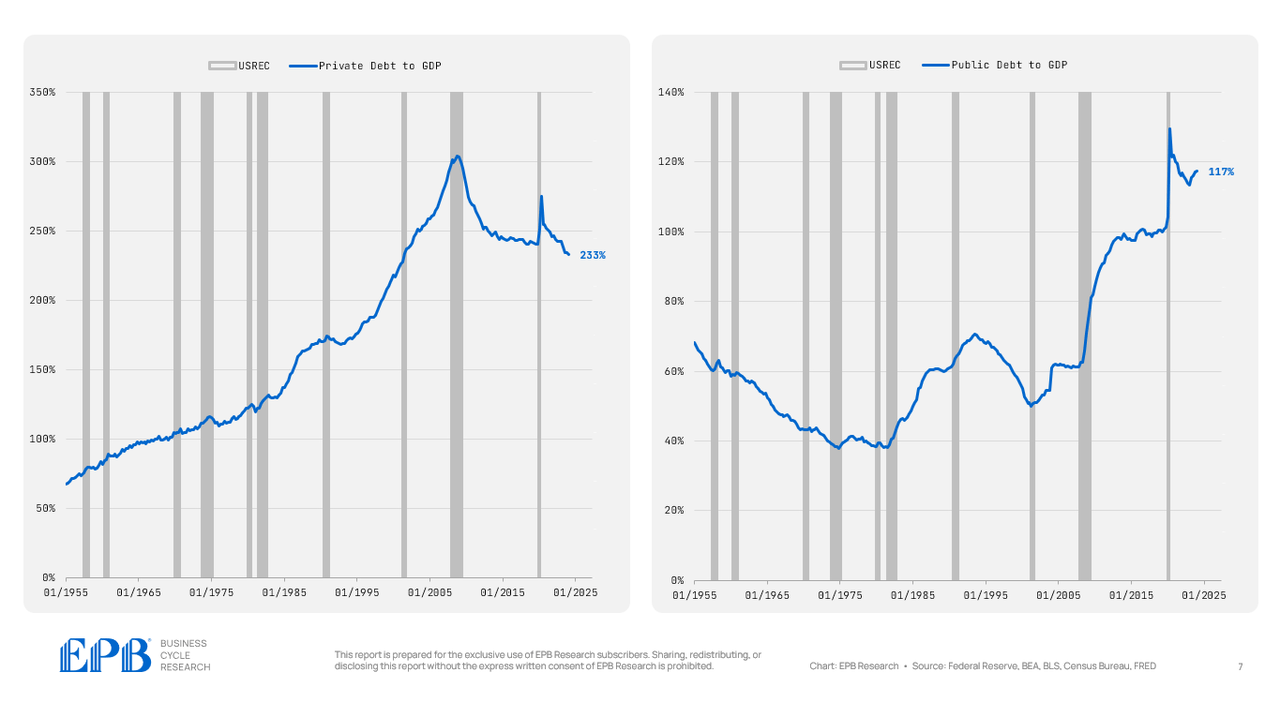

If we go one layer deeper, and we analyze non-public sector debt and authorities sector debt, we are able to see some modifications.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

The non-public sector which incorporates the enterprise sector, family sector and monetary sector, has a complete debt to GDP stage of 233% in comparison with a median of 245% from 2012 to 2019 and 290% in 2007.

So, the non-public sector has decreased its debt burden, however on the flip facet, the federal government sector has 117% debt to GDP, a rise from 99% from 2012 to 2019 and 61% in 2007.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So there was no internet discount in debt burden throughout the whole financial system, we merely shifted debt from the non-public sector steadiness sheet to the federal government steadiness sheet, conserving mixture debt ranges nearly precisely the identical.

Let’s dig one layer deeper, beginning with public debt, which is comprised of the federal authorities and the state & native governments.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So we all know the entire authorities sector has massively elevated debt during the last a number of years, as much as a complete of 117% of GDP as of the beginning of 2024.

Nearly all of this debt is being pushed by the federal authorities, which has a debt burden of 106% to begin 2024, in comparison with a median of simply 41% in 2007.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

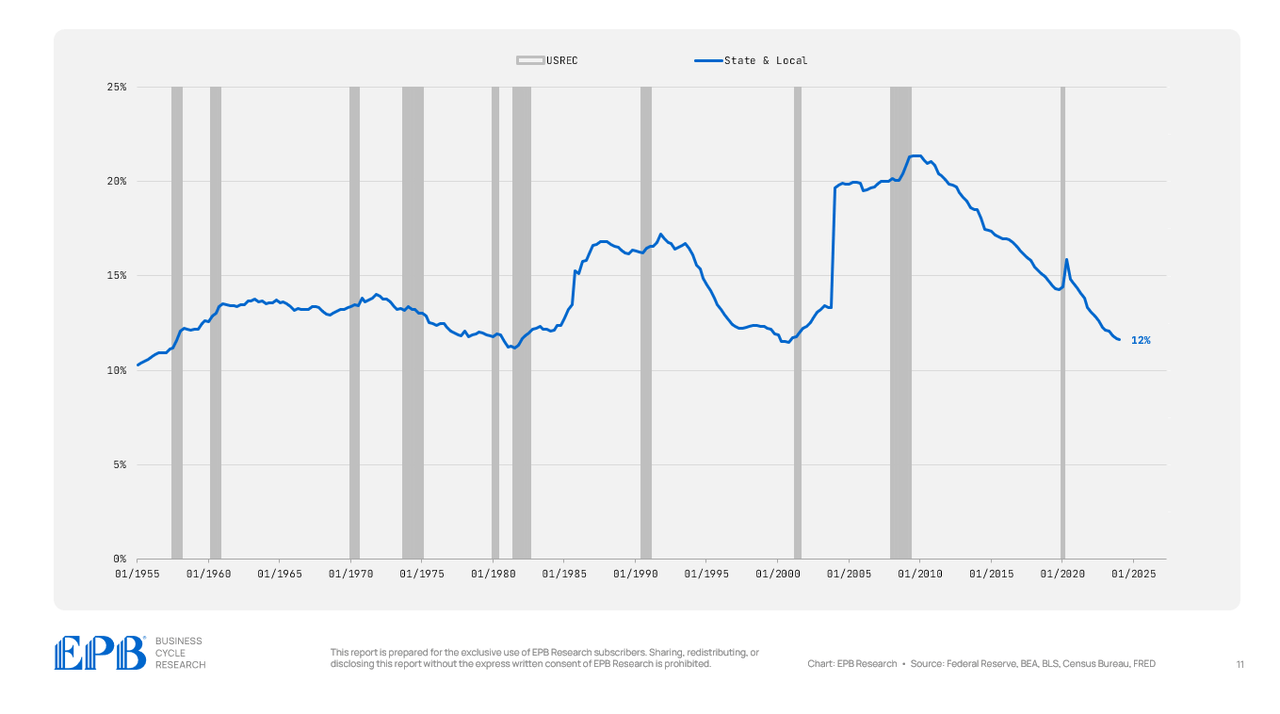

The state and native authorities debt burden has truly decreased fairly dramatically, falling to only 12%.

Now, this doesn’t imply state and native governments are being extra fiscally accountable; relatively, we’re simply rolling the debt as much as the federal sector by the federal authorities offering help to state and native governments.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

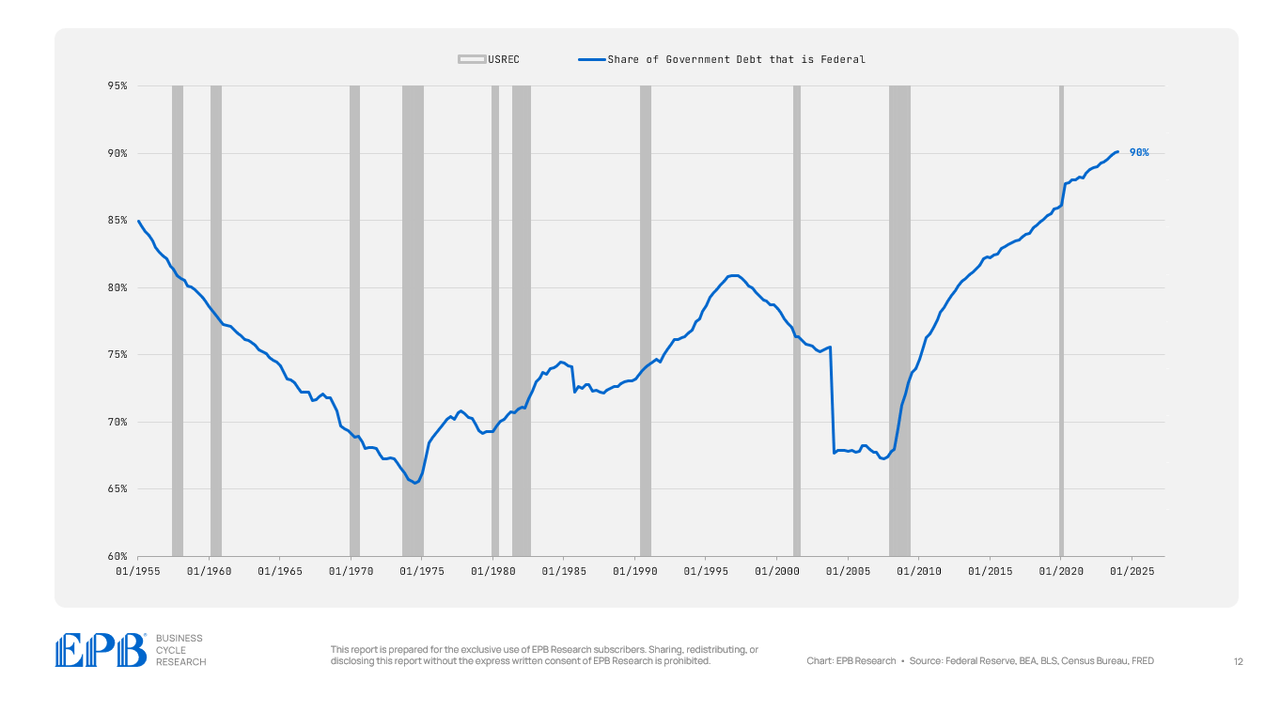

We’re concentrating extra debt or spending on the federal stage.

In 2007, roughly 65% of presidency debt was federal debt. Right now, nearly 90% of presidency debt is federal debt.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So not solely are we shifting debt from the non-public sector to the general public sector, we’re rolling all of the debt upwards to the federal authorities steadiness sheet.

In order we preserve referencing this debt map, we are able to mark the place the debt buildup is. We haven’t decreased complete debt in any respect since 2007, however we’ve shifted debt to the general public sector and extra particularly to the federal authorities.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

Let’s now transfer to the non-public sector and have a look at the three main sectors: the enterprise sector, the monetary sector, and the family sector. The combination non-public sector is in higher form than in 2007, however there are completely troubled pockets.

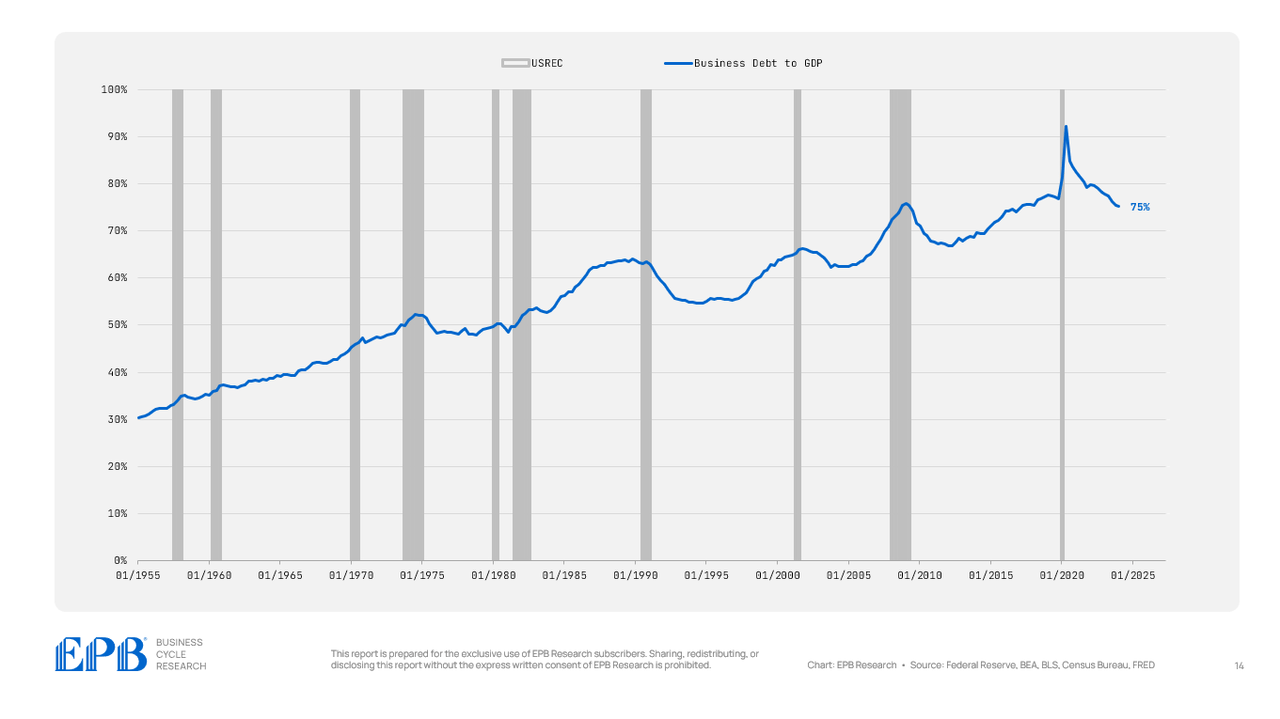

The enterprise sector, which incorporates company and noncorporate companies, presently holds a debt stage equal to 75% of GDP, greater than the 73% averaged from 2012 to 2019 and the 69% averaged in 2007. So, the general enterprise sector stays extremely leveraged.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

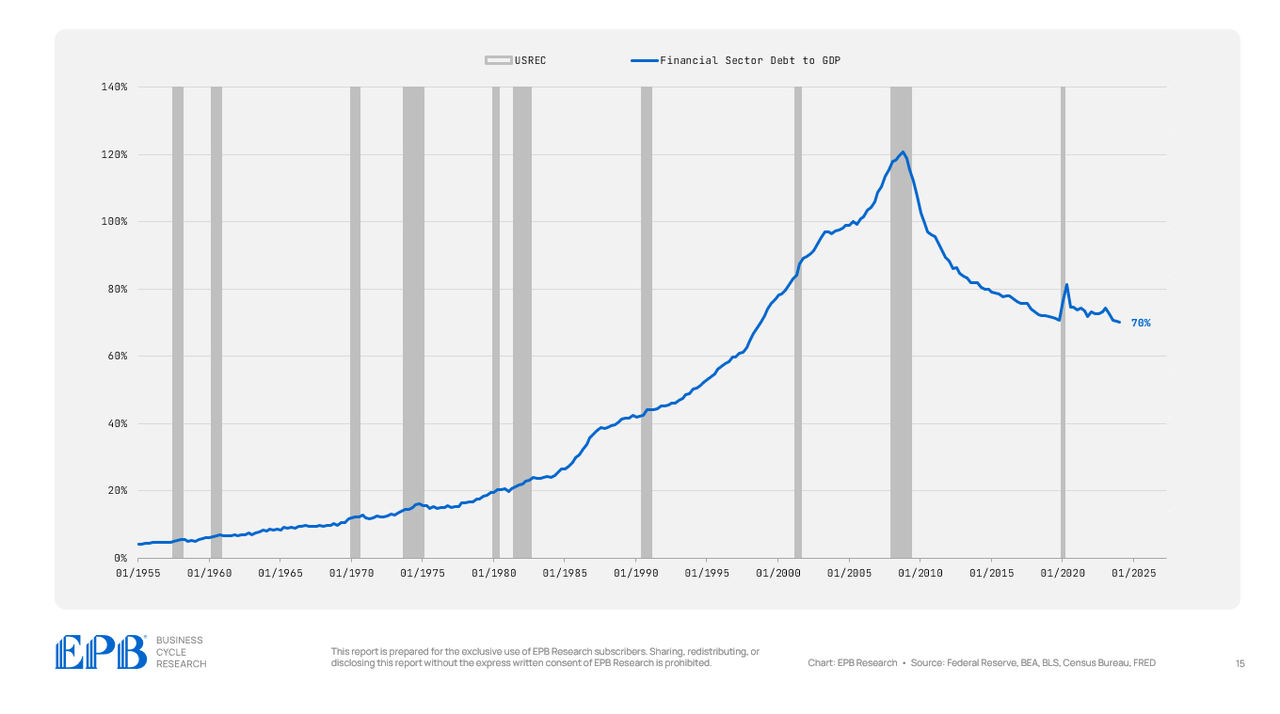

The monetary sector was one of many main sources of bother within the 2007 disaster, with common debt ranges equal to 112% of GDP in comparison with 70% at present. So the monetary sector deleveraged in a giant approach.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

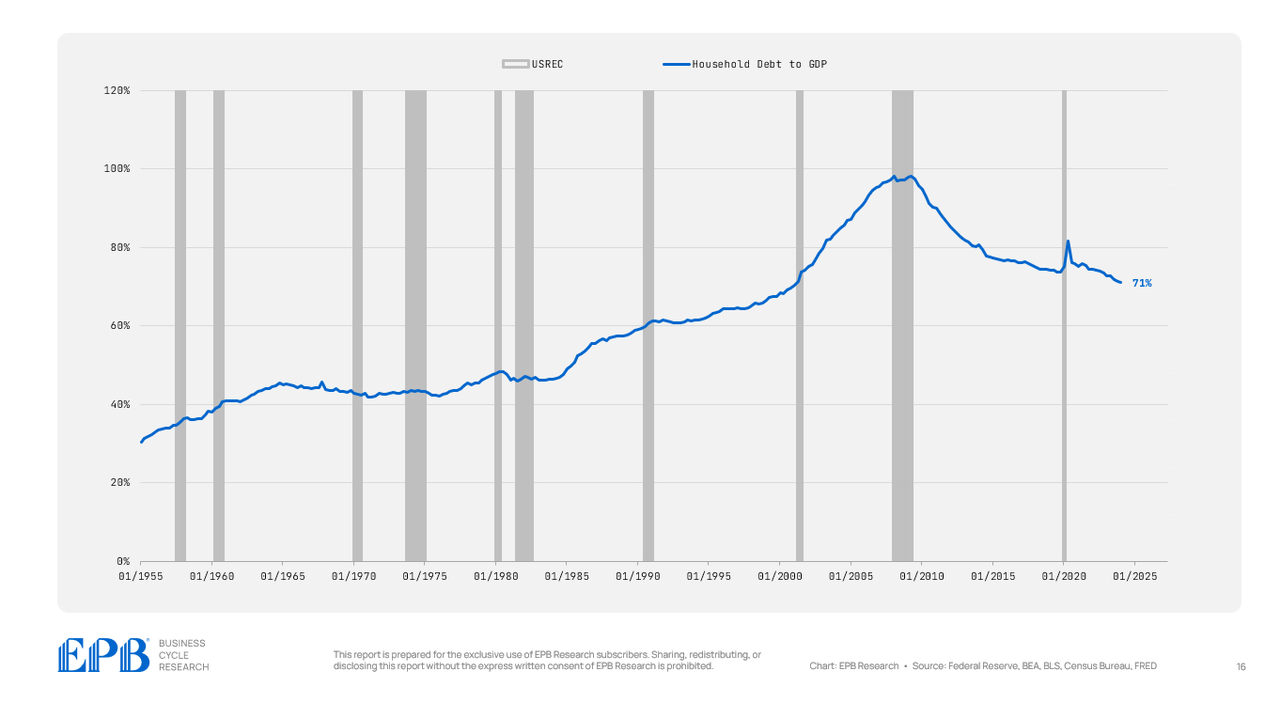

The family sector additionally deleveraged with a debt stage of 71% of GDP at present in comparison with nearly 100% in 2007.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So the entire non-public sector deleveraged whereas the general public sector massively elevated leverage.

Inside the non-public sector, the monetary sector and family sector decreased debt whereas the enterprise sector maintains a really extremely leveraged place.

Let’s now transfer one layer deeper throughout the enterprise and family sectors.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

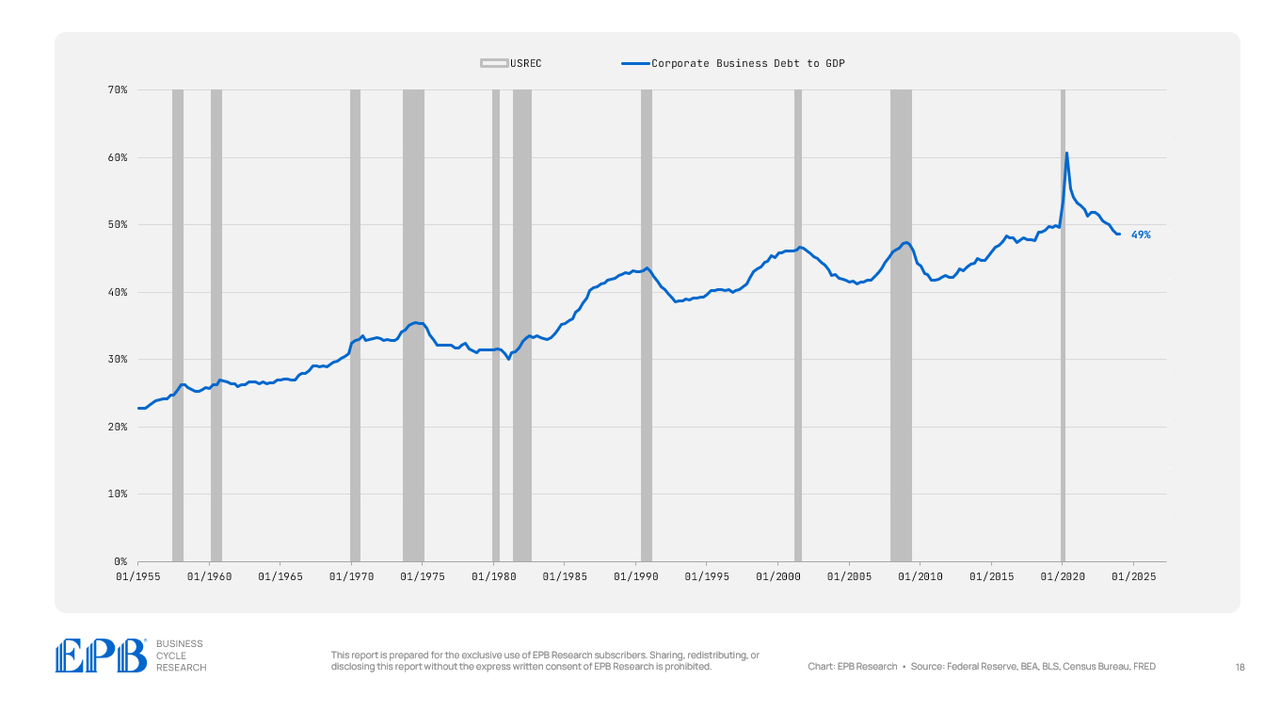

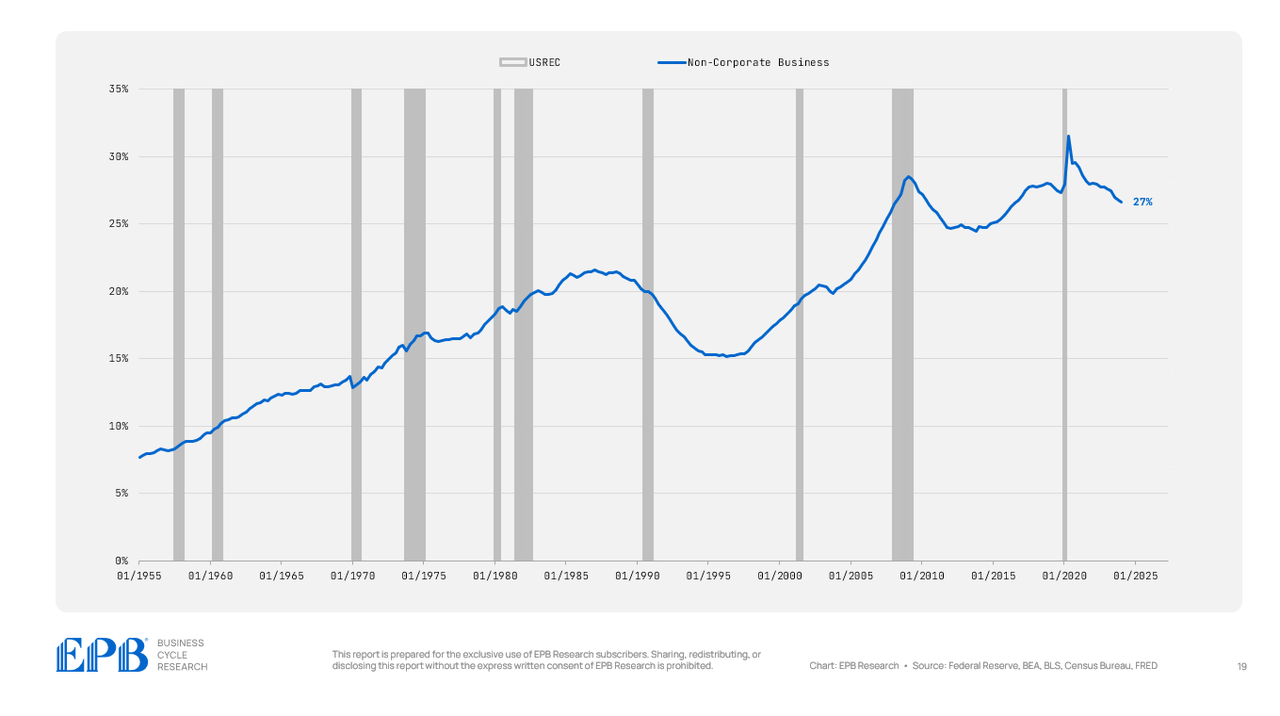

The enterprise sector is made up of company and non-corporate companies.

There’s no materials distinction between the company and non-corporate sectors – each have maintained a extremely leveraged place. The company sector has a debt stage of 49% of GDP in comparison with 44% in 2007.

The non-corporate enterprise sector has a debt stage of 27% of GDP at present in comparison with 25% in 2007.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So, throughout the enterprise sector, which is holding one of many highest debt burdens of all time, each the company and non-corporate sectors are contributing to the shortage of deleveraging.

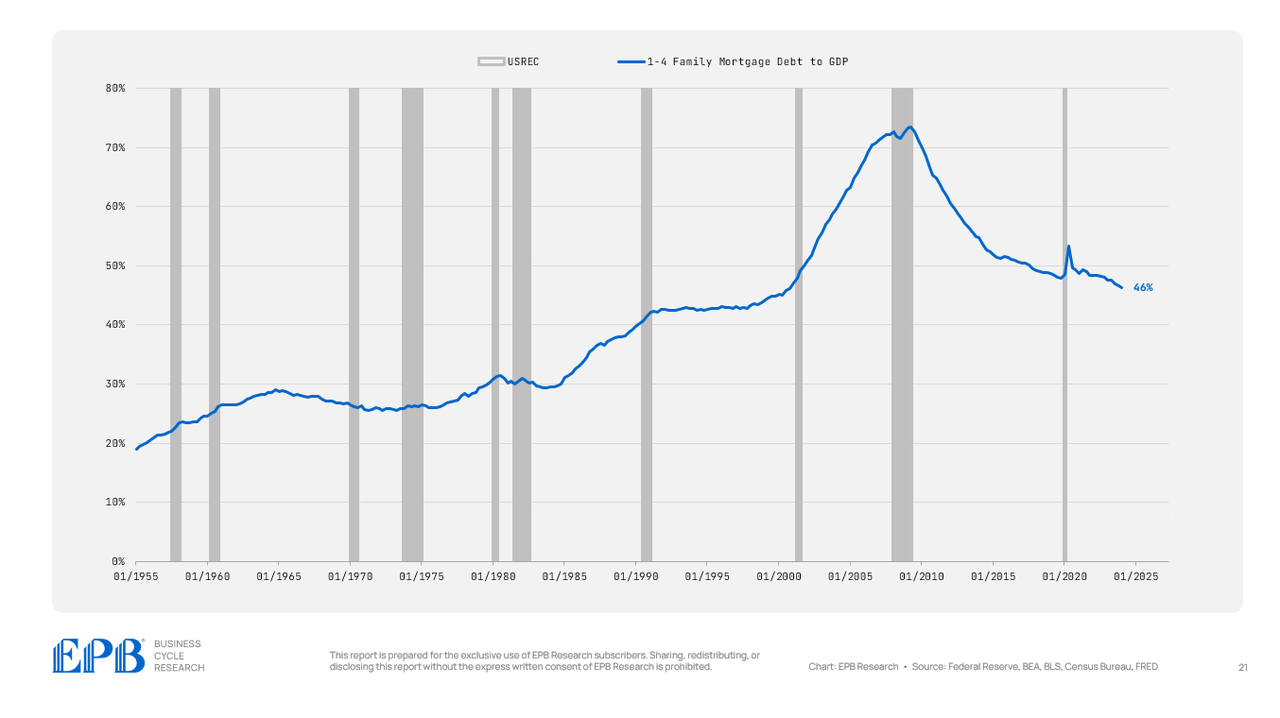

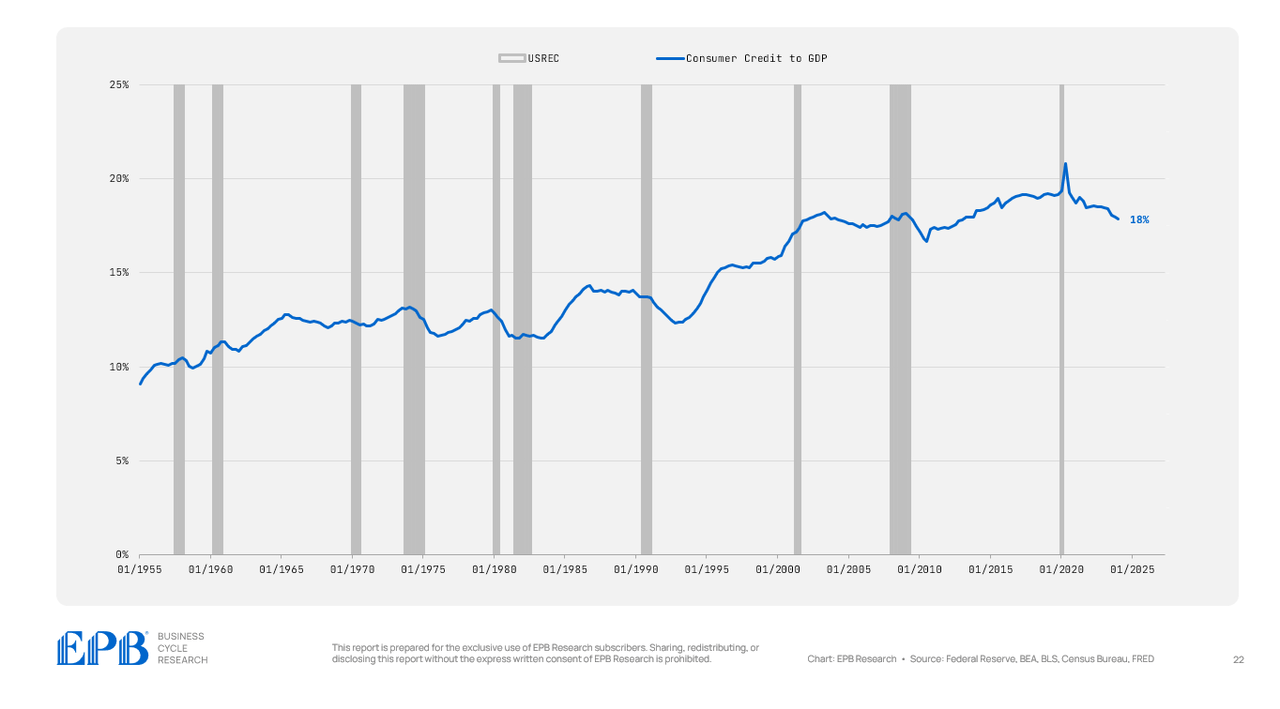

Family debt is made from two main classes, mortgage debt and client debt.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

Let’s check out the fourth layer of our debt map for the family sector.

Mortgage debt has been dramatically decreased within the family sector, falling from 72% of GDP in 2007 to 52% within the 2012 to 2019 interval to 46% at present.

The family sector massively decreased mortgage debt.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

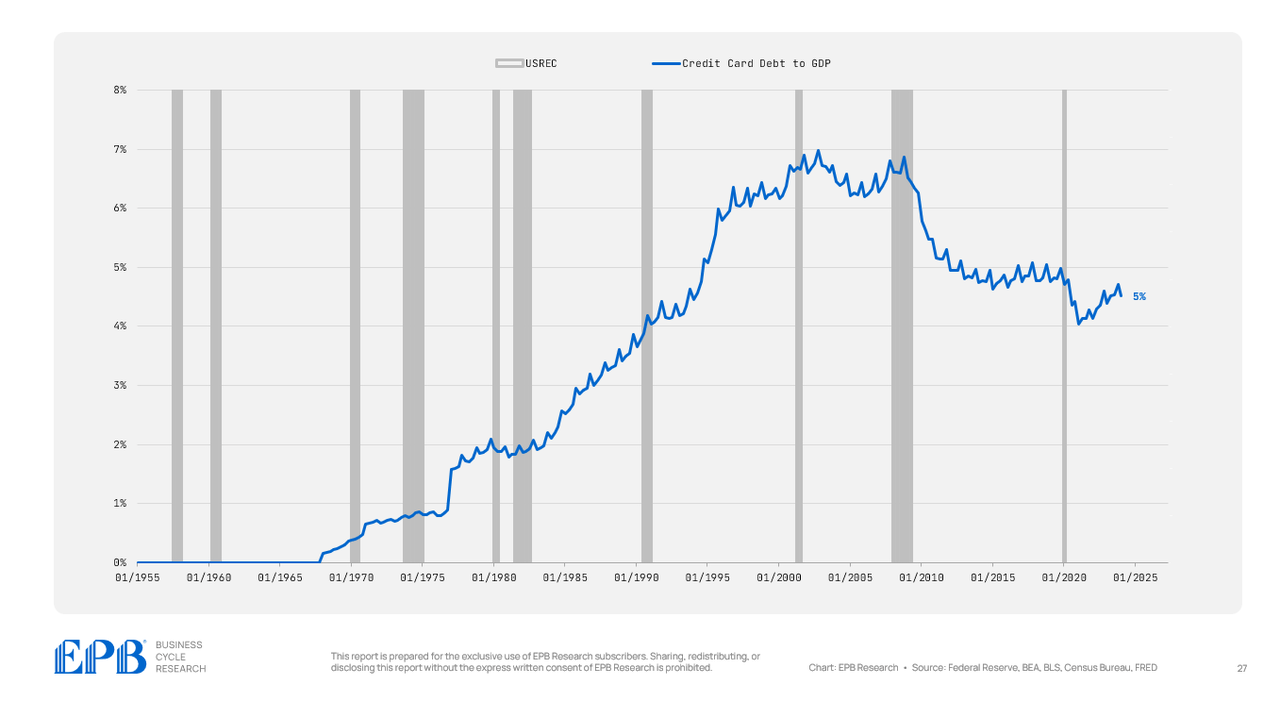

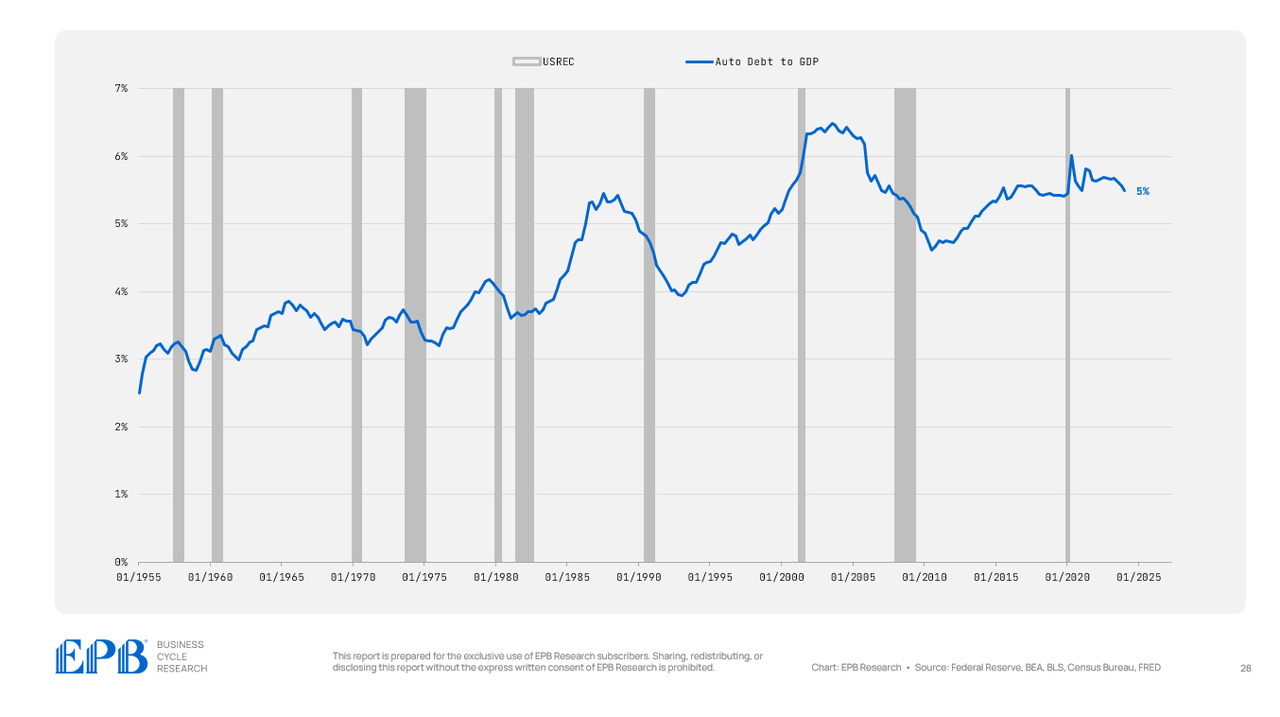

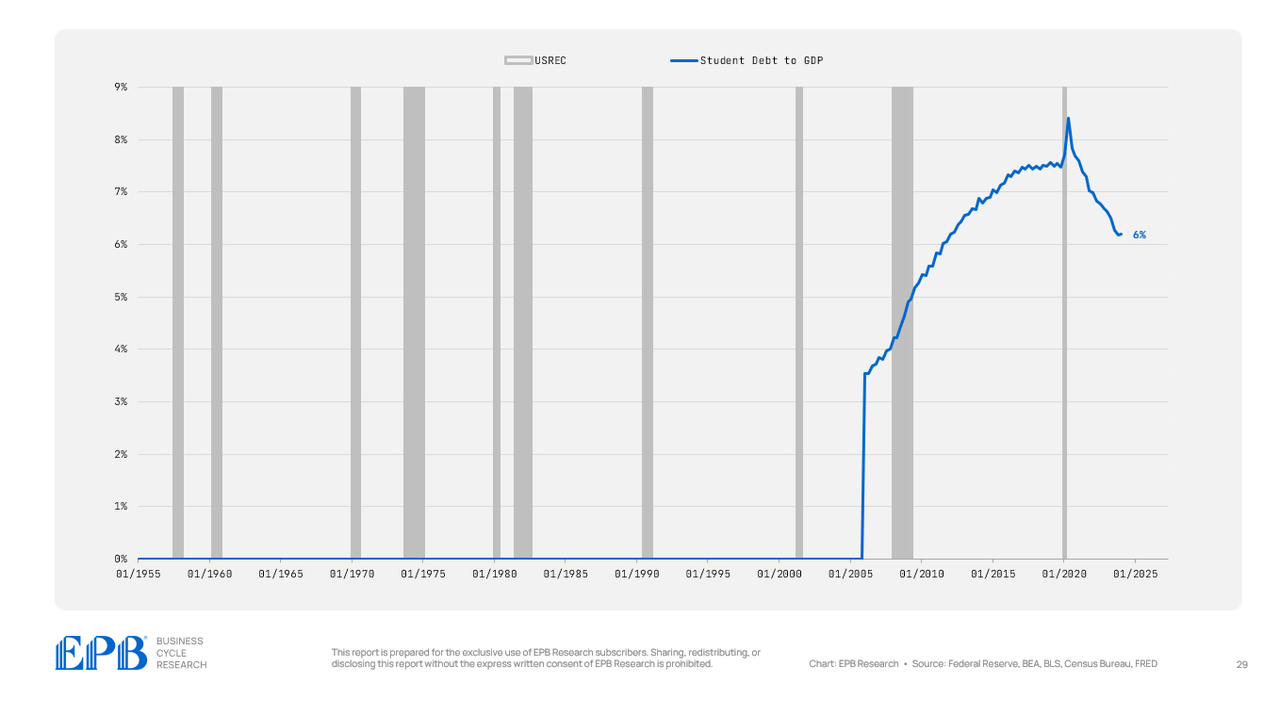

Client debt, alternatively, which is scholar loans, auto loans, and bank card loans, is eighteen% at present in comparison with nearly the identical stage in 2007 and the typical from 2012 to 2019.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So what’s occurred within the family sector is mortgage debt dropped sharply and client debt remained very elevated.

Wealthier households have extra mortgage debt, and lower-income households have extra client debt. So wealthier households have possible deleveraged however decrease earnings households stay below a particularly excessive stage of client debt.

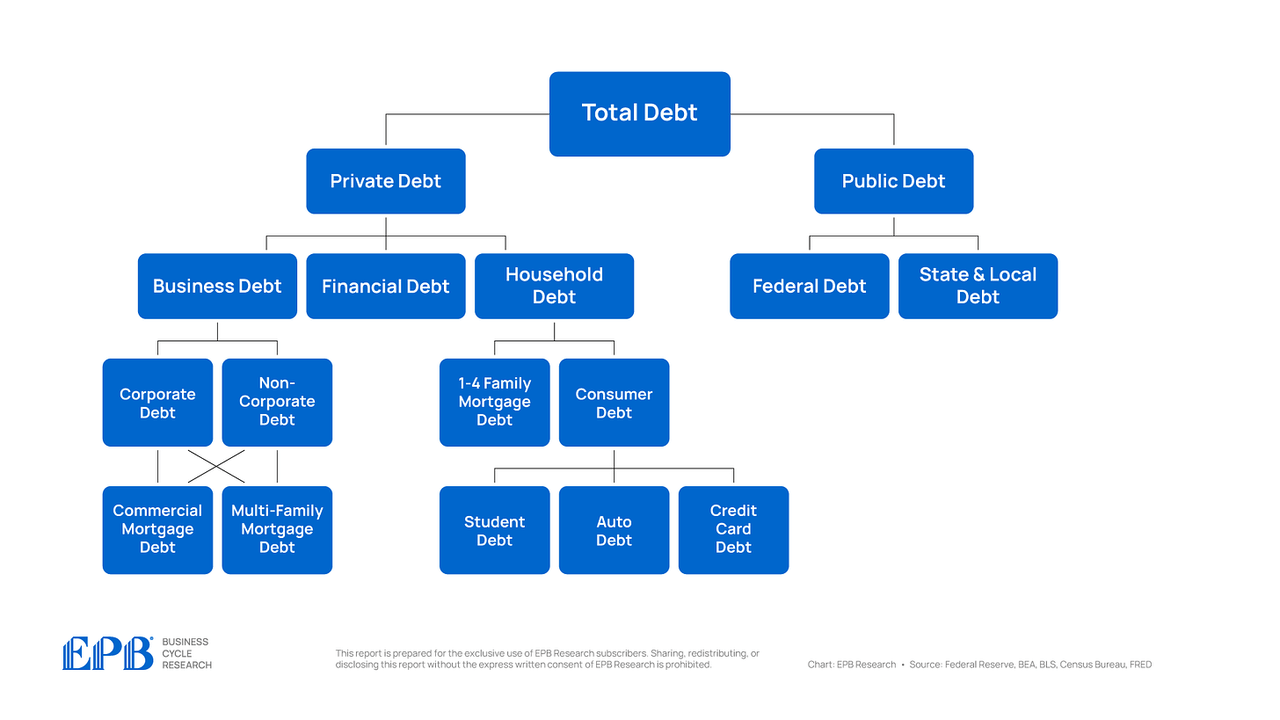

Let’s now transfer to the fifth layer in our chart and have a look at the enterprise sector which holds each industrial mortgage debt and multi-family mortgage debt.

Industrial and multi-family debt are held by each the company and noncorporate sectors typically.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

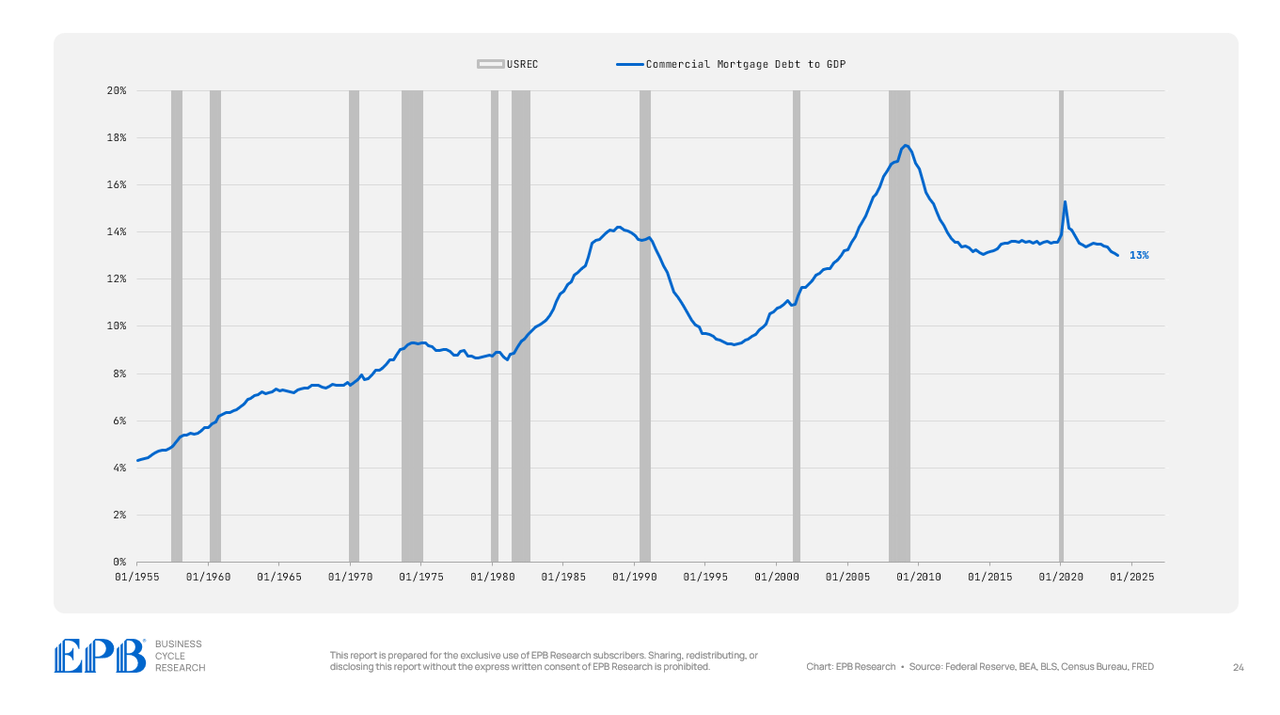

Industrial mortgage debt has declined lately, averaging 16% of GDP in 2007 in comparison with 13% at present.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

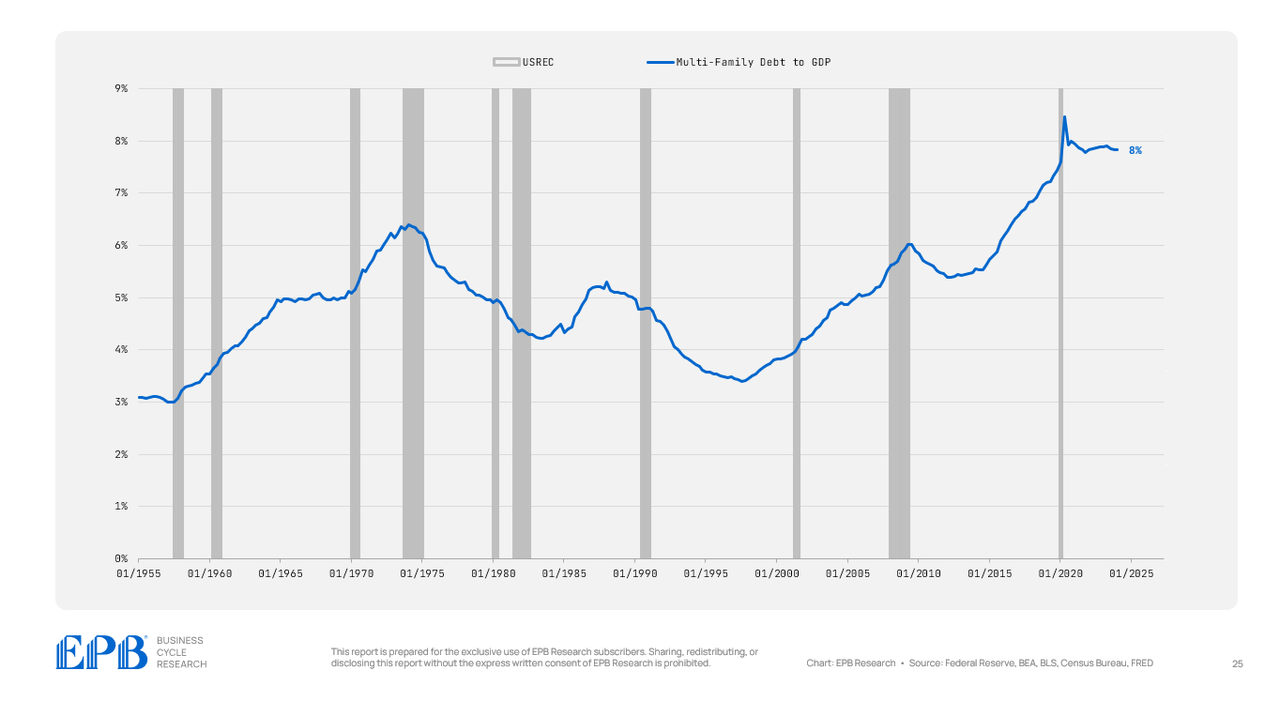

Multi-family debt, nevertheless, has been probably the most aggressive run-ups of any sector thus far.

Multi-family mortgage debt fueled an enormous overbuilding of flats with debt within the sector now at 8% of GDP in comparison with 5% in 2007. The present stage of multi-family mortgage debt is the very best stage in historical past for the US.

That is clearly one of many downside areas for this financial cycle, as some individuals will likely be holding multi-family debt in opposition to overbuilt properties that weren’t good investments.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So we now know that throughout the enterprise sector, multi-family debt is without doubt one of the downside areas, and it’s held by each company and noncorporate companies, in addition to smaller segments of the monetary sector like regional banks.

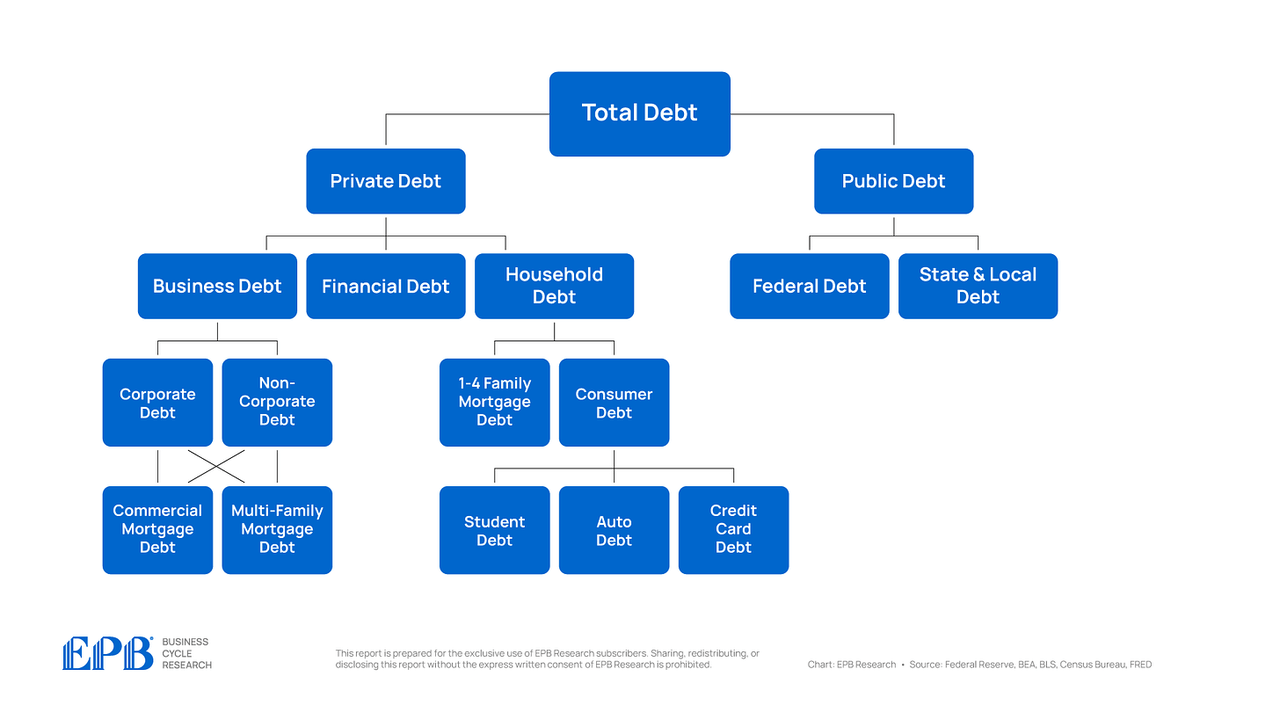

Let’s wrap up by trying on the fifth layer of our debt map however for the family sector that are the three main segments of client debt.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

As a proportion of GDP, bank card debt has declined for the reason that 2007 interval, however auto debt has remained at very elevated ranges, holding round 5% of GDP.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

Pupil debt has exploded during the last 20 years, nevertheless it has declined after the pandemic, now at 6% of GDP.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

So after we visible the whole US debt map, and break it into 5 layers, we are able to establish the issues areas and the possible supply of private and non-private sector stress.

The entire US debt state of affairs stays simply as unmanageable as 2007, or the pre-pandemic interval.

BEA, BLS, Federal Reserve, Census Bureau, EPB Analysis

The non-public sector as an entire is in a lot better share than it has been during the last 20 years on common however the public sector is in far worse share with an growing share of that debt burden, which as much as 90%, has shifted particularly to the federal authorities.

Inside the non-public sector, there are some pockets of elevated debt burden. The company and noncorporate sector have a excessive stage of multi-family house mortgage debt. There was enormous overbuilding in multi-family flats during the last 10-15 years and it’s clear that a few of this multi-family mortgage debt is dangerous debt that may trigger losses. There’s all the time dangerous debt when leverage will increase quickly.

The family sector has a decrease debt burden in comparison with the final 20 years nevertheless it’s all from a discount in mortgage debt. Client debt burdens stay simply as excessive as ever within the final 20 years, with scholar loans and auto loans being the most important culprits.

Larger authorities debt, will proceed to scale back the usual of residing for the typical American and throughout the non-public sector, we must be most targeted on the buildup of debt throughout the multi-family sector, principally owned by regional banks and personal fairness funds.

[ad_2]

Source link

")

")

")

")

{kind=link}