[ad_1]

The way to Enhance Commodity Momentum Utilizing Intra-Market Correlation

Momentum is likely one of the most researched market anomalies, well-known and extensively accepted in each public and tutorial sectors. Its idea is easy: purchase an asset when its worth rises and promote it when it falls. The purpose is to benefit from these traits to realize higher returns than a easy buy-and-hold technique. Sadly, over the past a long time, we have now been observers of the diminishing returns of the momentum methods in all asset courses. On this article, we’ll current an intra-market correlation filter that may assist considerably enhance commodity momentum efficiency and return this technique as soon as once more into the highlight.

Whereas early momentum analysis primarily centered on shares, related patterns have been recognized throughout numerous asset courses. As an example, our Quantpedia Screener lists a momentum technique particularly for commodity futures. The technique entails rating the commodity futures by efficiency over the previous 12 months and dividing them into quintiles. The highest-performing quintile is purchased, and the bottom-performing quintile is bought, with rebalancing going down every month.

In Quantpedia’s analysis titled “What’s the Finest Issue for Excessive Inflation Intervals?“, the momentum impact was discovered to be constructive in periods of excessive inflation round World Struggle II and the Oil Disaster of 1973. Nonetheless, lately, the efficiency of momentum methods has declined. Momentum has struggled to successfully distinguish between winners and losers in homogeneous funding universes, as totally analyzed within the current Quantpedia analysis paper titled “Robustness Testing of Nation and Asset ETF Momentum Methods”. The findings recommend that momentum methods carry out higher in asset-based ETFs than in country-based ETFs as a result of decrease correlation between belongings.

Constructing on these insights, this paper goals to handle the current decline in momentum efficacy by exploring methods to implement momentum in homogeneous commodity ETFs, relatively than commodity futures. First, we take a look at a primary momentum technique, which doesn’t produce important alpha. Subsequent, we enhance the essential technique by utilizing the ratio of short-term to long-term common correlations as a sign for when it’s favorable to use momentum methods, yielding promising outcomes. We suggest a method based mostly on this intra-market correlation filter.

Methodology and Information

For this evaluation, we selected sector commodity ETFs on account of their ease of use, size of knowledge, accessibility, and no want for complicated rolling procedures. The technique focuses on 4 sector-specific commodity ETFs: DBA (agriculture), DBB (base metals), DBE (vitality), and DBP (valuable metals). These ETFs provide an extended backtesting interval, ranging from 2007, in comparison with particular person commodity ETFs. Information had been sourced from Yahoo Finance, utilizing the adjusted shut costs (adjusted for inventory splits, dividend distributions, and different related occasions affecting inventory’s worth) for the chosen ETFs. From the each day information, we calculated each each day and month-to-month efficiency.

Step 1

Step one was to duplicate a easy momentum technique utilizing the 4 ETFs (DBA, DBB, DBE, and DBP). Every month, we calculated the 1- to 12-month momentum for every ETF and ranked them based mostly on their efficiency. This rating supplied the indicators for which ETFs to go lengthy and which to quick. The technique concerned going lengthy on the 2 best-performing ETFs and quick on the 2 worst-performing ones mimicking the essential premise of momentum that winners will proceed to outperform and losers will proceed to underperform. The portfolio was equally weighted and rebalanced on a month-to-month foundation.

Outcomes of step 1

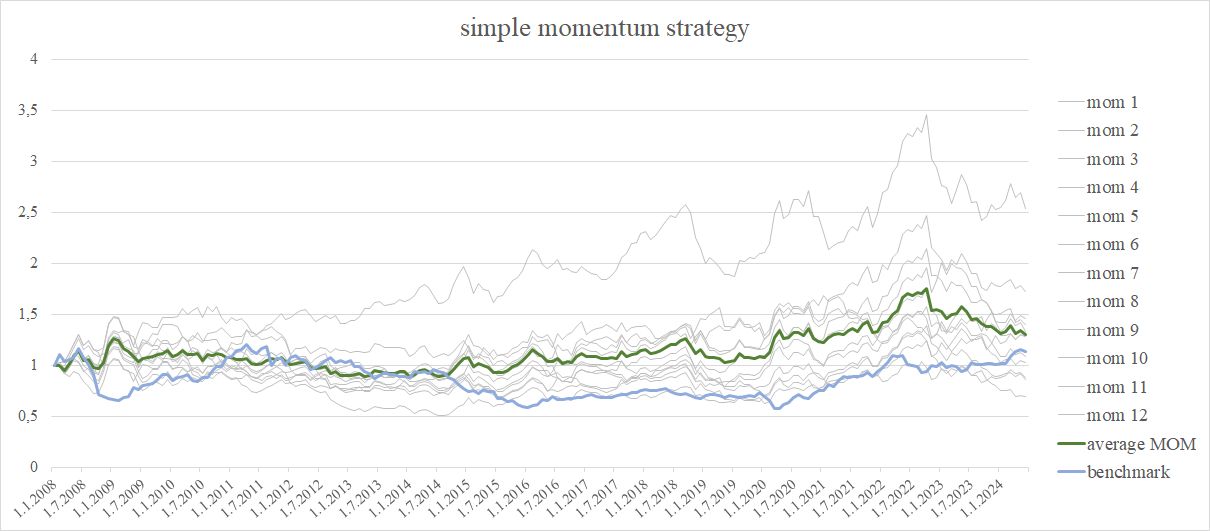

Desk 1 easy momentum traits

Determine 1 easy momentum technique

As anticipated, the momentum technique on commodities yielded poor efficiency. Desk 1 reveals that whereas it barely outperforms the benchmark return, this comes at the price of greater volatility. This consequence aligns with earlier analysis, together with analysis by Quantpedia. In homogeneous markets like commodities, the place belongings are extremely correlated, momentum struggles to successfully differentiate between winners and losers, resulting in disappointing efficiency.

One potential manner to enhance efficiency of momentum methods in commodity ETFs is by turning to low-liquidity belongings. In considered one of Quantpedia’s earlier research “The way to Use Unique Belongings to Enhance Your Buying and selling Technique”, the authors examined the illiquidity premium—the concept that anticipated returns enhance with illiquidity—by operating a set of momentum methods utilizing commodity futures contracts from two main commodity indices, S&P GSCI and BCOM. The outcomes confirmed that non-indexed, or unique, low-liquidity belongings outperformed listed ones, providing greater returns with almost the identical danger as listed commodity methods.

Step 2

Whereas turning to low-liquidity belongings was one possibility, we determined to discover other ways to make momentum methods work successfully in commodity ETFs. Our purpose was to discover a dependable predictor that might sign when it’s favorable to use a momentum technique and when it’s not. We quickly found that the ratio of short-term to long-term correlation might function such a predictor.

The following step in our evaluation concerned calculating common short-term (measured over 20 days) and aveage long-term (measured over 250 days) correlations from the each day efficiency of the 4 ETFs. If the typical short-term correlation exceeds the typical long-term correlation between ETFs, it signifies that commodities are trending in a single course, permitting momentum methods to extra successfully distinguish between winners and losers. Deploying momentum beneath these situations can subsequently be extra worthwhile. In abstract, correlation filter permits us to use the momentum technique selectively, utilizing it solely when market situations are favorable.

Outcomes of step 2

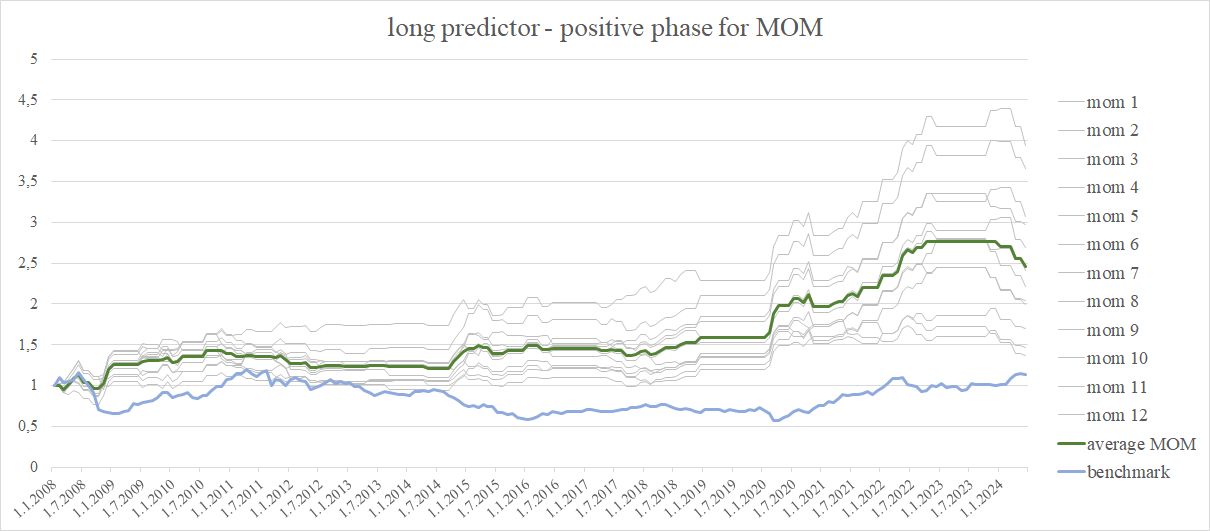

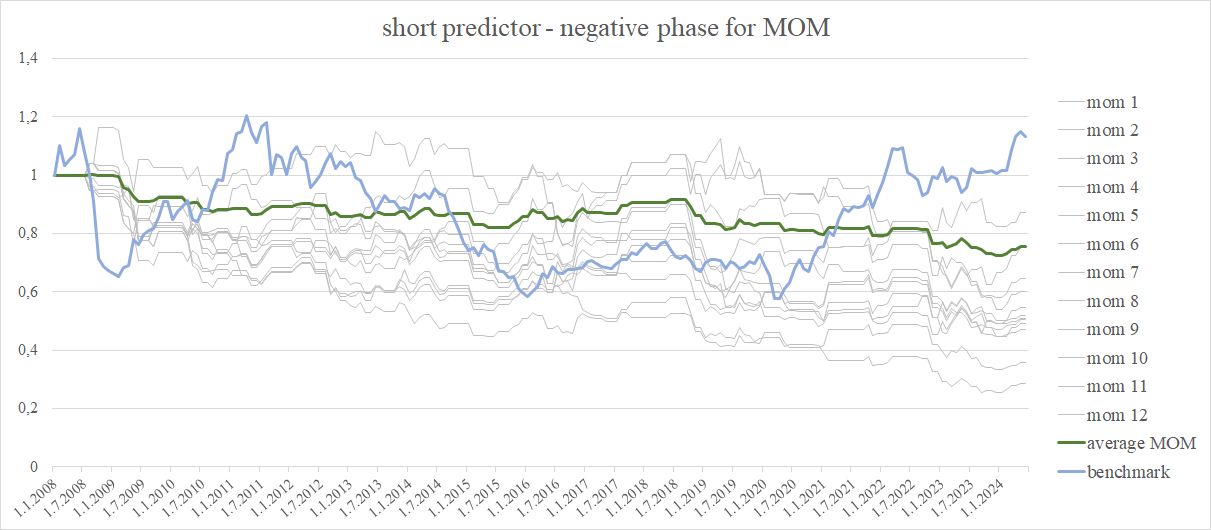

As proven in Desk 2, the correlation predictor results in extra pleasing outcomes in comparison with the essential momentum technique. It outperforms the momentum technique throughout all efficiency metrics, together with annual returns, volatility, most drawdown, Sharpe ratio, and Calmar ratio. The correlation filter seems to be fairly strong. Whatever the momentum rating interval (1-12 months), the filter reliably identifies when it’s applicable to commerce the momentum technique (determine & desk 2) and when it’s extra appropriate to commerce the reversal impact because the momentum technique persistently yields destructive outcomes (determine & desk 3).

Desk 2 lengthy predictor traits

Determine 2 lengthy predictor

Desk 3 quick predictor traits

Determine 3 quick predictor

Step 3

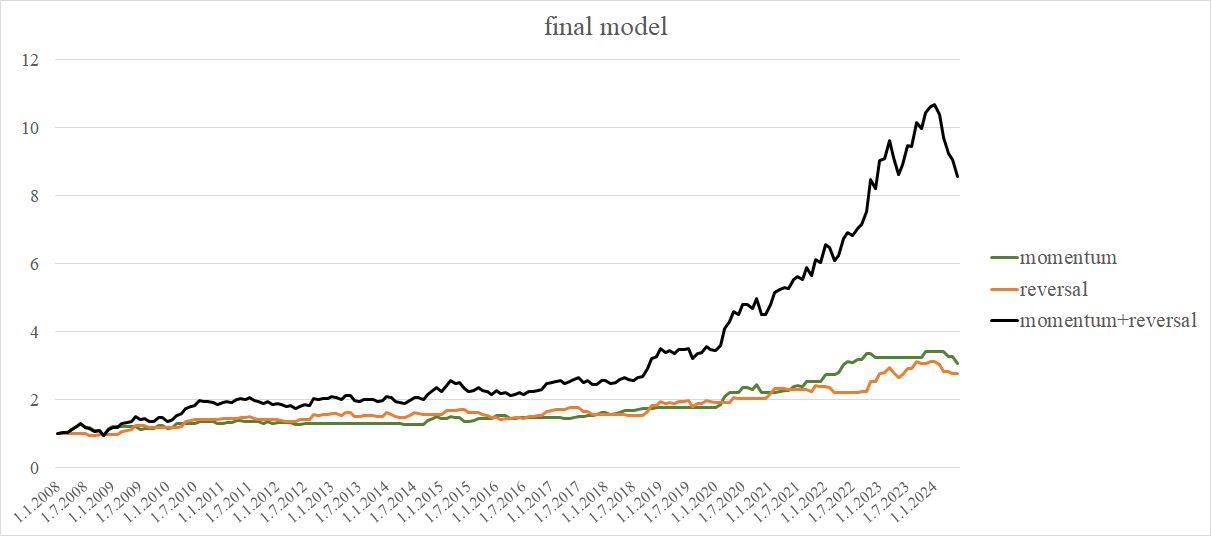

The insights gained from this analysis open the door for the event of recent, thrilling methods. Based mostly on these findings and present literature, we suggest the next technique utilizing a correlation filter: if the short-term correlation is greater than the long-term correlation, apply the momentum technique by going lengthy on the two best-performing and quick on the two worst-performing sector commodity ETFs, based mostly on a 12-month rating, and maintain the positions for 1 month. If the short-term correlation is decrease than the long-term correlation, apply a reversal technique by going lengthy on the two worst-performing and quick on the two best-performing sector commodity ETFs (based mostly on a 12-month rating), and maintain the positions for 1 month. As proven in Determine 4 and supported by the ends in Desk 4, this mixed technique (Mother+Rev) almost doubles the return of both the standalone momentum or reversal methods. Though the upper volatility and most drawdown recommend an elevated degree of danger, this can be justified by the considerably greater returns.

Desk 4 steered technique traits

Determine 4 steered technique

Conclusion

On this paper, we addressed the challenges of momentum in homogeneous markets like commodities utilizing extensively accessible sector commodity ETFs.

In abstract, whereas a primary momentum technique utilized to commodities yields disappointing outcomes, incorporating a predictor based mostly on intra-market correlation considerably enhances momentum technique’s efficiency. This ratio between 20-day and 250-day correlation offers a dependable sign figuring out when commodities are trending strongly sufficient for momentum to tell apart between winners and losers.

Writer: Margareta Pauchlyova, Quant Analyst, Quantpedia

References

Quantpedia. (n.d.). Momentum impact in commodities. Retrieved September 1, 2024, from https://quantpedia.com/methods/momentum-effect-in-commodities/

Quantpedia. (n.d.). What’s the perfect issue for top inflation intervals? (Half II). Retrieved September 1, 2024, from https://quantpedia.com/whats-the-best-factor-for-high-inflation-periods-part-ii/

Du, Jiang and Vojtko, Radovan, Robustness Testing of Nation and Asset ETF Momentum Methods (March 25, 2023). Obtainable at SSRN: https://ssrn.com/summary=4736699 or http://dx.doi.org/10.2139/ssrn.4736699

Cisár, Dominik and Vojtko, Radovan, The way to Use Unique Belongings for Buying and selling Technique Enchancment (September 3, 2021). Obtainable at SSRN: https://ssrn.com/summary=3916918 or http://dx.doi.org/10.2139/ssrn.3916918

Are you on the lookout for extra methods to examine? Go to our Weblog or Screener.

Do you need to be taught extra about Quantpedia Professional service? Verify its description, watch movies, evaluate reporting capabilities and go to our pricing provide.

Do you need to know extra about us? Verify how Quantpedia works and our mission.

Are you on the lookout for historic information or backtesting platforms? Verify our listing of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a pal

[ad_2]

Source link

, Boeing (NYSE:BA)")

{kind=link}