[ad_1]

Up to date on June twenty eighth, 2024 by Bob Ciura

Antero Midstream (AM) inventory at the moment has a horny dividend yield of 6.0%. It is among the high-yield shares in our database.

We have now created a spreadsheet of shares (and intently associated REITs and MLPs, and many others.) with dividend yields of 5% or extra.

Antero is a part of our ‘Excessive Dividend 50’ sequence, the place we cowl the 50 highest yielding shares within the Certain Evaluation Analysis Database.

You may obtain your free full checklist of all excessive dividend shares with 5%+ yields (together with necessary monetary metrics equivalent to dividend yield and payout ratio) by clicking on the hyperlink beneath:

On this article, we’ll analyze the prospects of Antero Midstream.

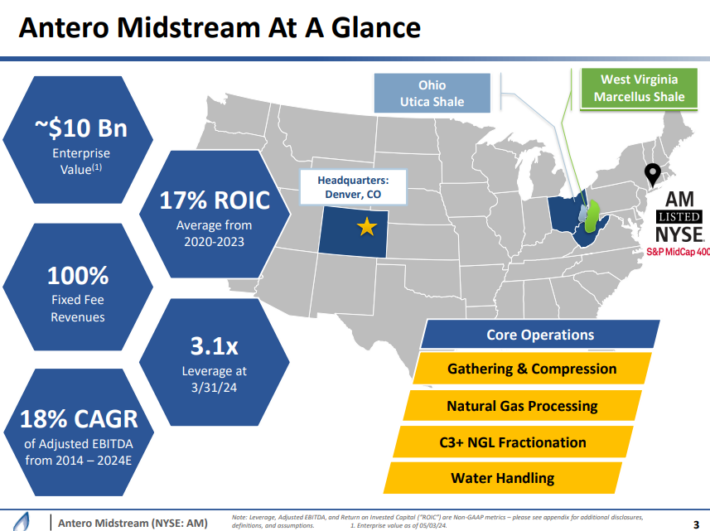

Enterprise Overview

Antero Midstream Company is a midstream firm offering gathering and compression, processing and fractionation, and pipeline providers on a captive foundation to Antero Assets (AR).

AR is the fifth largest pure fuel producer and 2nd largest NGL producer within the nation, working fields primarily in West Virginia.

As appears typical for these midstream companies, the publicly traded entity is a pass-through for the income from the underlying working entity.

Supply: Investor Presentation

Within the 2024 first quarter, Antero Midstream’s gathering and processing volumes elevated 4% and 6% respectively in comparison with the prior 12 months quarter.

Internet earnings reached an organization document of $104 million, or $0.21 per diluted share, marking a 17% per share enhance from the earlier 12 months quarter.

Adjusted EBITDA additionally elevated by 10% in comparison with the prior 12 months quarter. Capital expenditures decreased by 11% from the prior 12 months quarter.

Income for the primary quarter was $279 million, with vital contributions from the Gathering and Processing section and the Water Dealing with section.

Development Prospects

Antero Midstream’s main progress catalyst transferring ahead is paying down its debt, which it plans to do aggressively within the coming years. Within the 2024 first quarter AM’s leverage declined to three.1x, down from 3.3x on the finish of 2023.

It has additionally accomplished a reasonably aggressive capital spending program and these tasks are actually coming on-line, producing elevated EBITDA.

It additionally could proceed to opportunistically pursue small progress tasks as they develop into obtainable to it by means of its shut partnership with Antero Assets.

Antero Midstream can also be investing in progress by means of optimizing its asset footprint.

Supply: Investor Presentation

For instance, within the first quarter the corporate positioned the Grays Peak compressor station into service with an preliminary capability of 160 million cubic toes per day.

In any other case, it would look to extend dividend per share payouts and/or purchase again shares if they continue to be attractively priced. Antero at the moment has a $500 million share repurchase authorization in place.

Shopping for again shares will function a progress catalyst by decreasing the overall share depend, thereby rising distributable money move per share over time.

Aggressive Benefits

Antero Midstream’s main aggressive benefits are present in its multi-decade underlying stock by way of its partnership with Antero Assets, its just-in-time method to capital investments, and its peer main returns on invested capital.

It’s the main midstream service supplier to Antero Assets, an organization with a premium core drilling stock that exceeds 20 years.

Its just-in-time and versatile capital funding philosophy helps it to attenuate dangers on its capital expenditures whereas additionally minimizing the time from spend to money move on its progress tasks.

In consequence, it is ready to generate constant and repeatable natural progress together with peer-leading returns on invested capital.

Dividend Evaluation

Antero Midstream is unlikely to develop its dividend in 2024, as administration is laser targeted on deleveraging the stability sheet proper now. Luckily, the corporate has no near-term maturities in 2024 or 2025.

As soon as it achieves its leverage goal of at or beneath 3.0x (anticipated by the top of 2024), it may enhance the dividend, or proceed to additional pay down debt, relying on market and business situations on the time.

Nevertheless, given the 6% present dividend yield, there isn’t any want for dividend progress to generate a horny yield, and the dividend seems to be fairly secure as effectively.

AM has a projected dividend payout ratio of 53% for 2024, which signifies a safe dividend.

Closing Ideas

Antero Midstream is among the most cost-effective C-Corp midstream corporations available in the market immediately, and likewise gives a really enticing dividend yield that seems secure for a few years to return.

It has a secure, commodity worth resistant money move profile with an extended demand timeline forward of it. Moreover, its predominant counter-party is quickly deleveraging its stability sheet, additional strengthening Antero Midstream’s security profile.

Whereas Antero Midstream is unlikely to be a speedy grower of its money move or its dividend within the coming few years, we view AM inventory as enticing for earnings buyers.

In case you are curious about discovering high-quality dividend progress shares and/or different high-yield securities and earnings securities, the next Certain Dividend sources might be helpful:

Excessive-Yield Particular person Safety Analysis

Different Certain Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to assist@suredividend.com.

[ad_2]

Source link

{kind=link}