[ad_1]

Within the mortgage price world, it’s generally a recreation of inches.

This may be true for each potential residence patrons and present householders searching for price reduction.

Granted, in case you’re that marginal in the case of affording a house, perhaps you must think about renting till it’s a little bit extra decisive.

However in case you already personal a house and maintain a excessive mortgage price, the following six months or so may make or break your refinance alternative.

Currently, mortgage charges have retraced from their latest lows of simply over 6%, returning to ranges round 6.625%.

Because of this, many thousands and thousands of house owners are now not “within the cash” for a refinance. However that would change right away, simply because it already has.

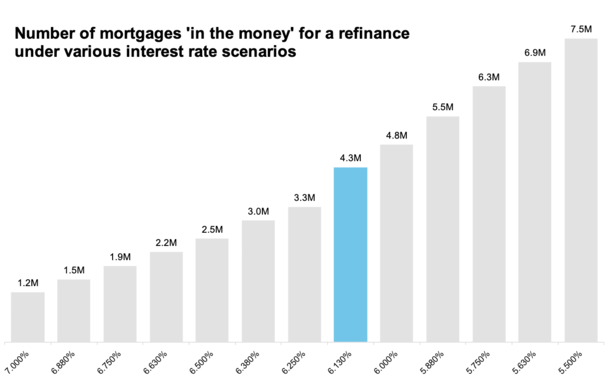

Are Present Mortgage Charges at Least 0.75% Under Your Charge?

A brand new report from ICE revealed that the refinance inhabitants climbed to over 4.3 million due to the rally in charges that got here to an abrupt finish, satirically after the Fed lower charges.

At the moment, the 30-year fastened mortgage was averaging round 6.125%, down from practically 7% as just lately as late July.

That meant the refinanceable inhabitants had surged from round 1.2 million to 4.3 million in a matter of lower than two months.

Of those 4.3M, a whopping 65% acquired their mortgages over the previous two years, together with 1.4M in 2023 and 1.3M this 12 months. In order that entire date the speed, marry the home factor may truly pan out.

ICE considers a home-owner “within the cash” for a price and time period refinance if their present mortgage price is at the least 0.75% beneath prevailing market charges.

So principally any borrower with a 7%+ price would have met that definition in mid-September.

However in the present day it’s solely the debtors with mortgage charges round 7.5% that might profit from a refi.

If you wish to get extra into the nitty-gritty, highly-qualified refinance candidates ought to have a 720+ FICO rating and a loan-to-value ratio (LTV) of 80% or much less.

In fact, circumstances can change rapidly. And as I wrote the opposite day, mortgage charges don’t transfer up or down in a straight line.

That means the latest uptick may simply be a short lived hiccup and short-lived. Mortgage charges noticed durations of reduction on the best way up. They may simply as effectively see durations of ache on the best way down.

The Refi Increase Relies on Charges Persevering with Decrease Into 2025

As you possibly can see, even minimal price modifications can affect thousands and thousands of house owners searching for fee reduction.

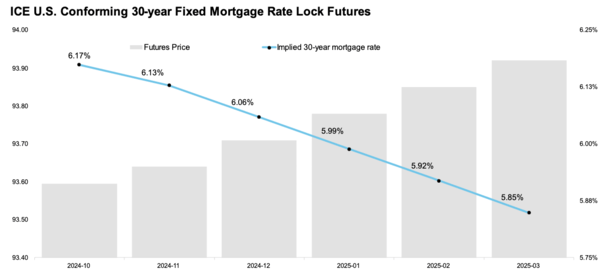

The excellent news is ICE expects 30-year fastened mortgage charges to proceed coming down into the final months of the 12 months and 2025. For the file, I agree with them.

Their newest estimate, calculated utilizing the single-day unfold between the mortgage steadiness weighted common APR futures worth and easy common each day price, has the 30-year down to five.85% by March 2025.

Granted it additionally has the 30-year fastened at 6.17% for October 2024, so some latest changes might haven’t been captured by their time-sensitive report.

However as famous, it’s good to zoom out anyway, and pay much less consideration to the day-to-day and even week-to-week noise.

Rather a lot can occur in a couple of days, and we’ve obtained two massive experiences coming tomorrow and Friday, the CPI report and PPI report.

Each may push charges again onto their downward trajectory. They may additionally push charges larger…

If ICE’s predictions maintain true longer-term, there shall be a pleasant little refi increase for mortgage officers and mortgage brokers in early 2025.

Charges may additionally method that so-called magic variety of 5.5%, at which level you’d get extra residence patrons getting into the market too, maybe simply in time for spring.

That is the bullish case for the mortgage market, however nonetheless very a lot up within the air. You may see simply how fickle all of it is with even a .125% or .25% distinction in price probably affecting thousands and thousands.

Learn on: The refinance rule of thumb.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on Twitter for decent takes.

[ad_2]

Source link

to report Q3 earnings on Oct 15. Here’s what to expect | AlphaStreet")

{kind=link}