[ad_1]

ermingut

Since our final replace in April, Supportive Outcomes – Purchase Confirmed, Exor N.V. (OTCPK:EXXRF)’s inventory value efficiency has not been best. As a reminder, the corporate reported a 2023 with a consolidated revenue of €4.2 billion and a 32.7% NAV per share improve. Our purchase score was supported by 1) an ongoing Buyback To Erase The NAV Low cost, 2) a 15% new funding in Philips (A Supportive Healthcare Acquisition) following the acquisition of the French Institut Mérieux, and three) the underlying strong efficiency of Stellantis and Ferrari. Following our evaluation, we see a couple of key takeaways value reporting, which help our forward-thinking view and speak in confidence to new situations.

Why are we nonetheless constructive?

(Exor continues to spend money on the healthcare area). Yesterday, the corporate determined to step up its investments in Philips. As a reminder, the corporate acquired a 15% fairness stake in August 2023. In accordance with paperwork filed on 25 June with the Safety and Change Fee (SEC), the holding firm elevated its stake, reaching 17.51%, a participation that’s now value over €3.5 billion. Exor would possibly improve its fairness stake by as much as 20%, and this newest transfer demonstrated confidence within the Dutch medical gadget participant. Exor is the corporate’s largest shareholder. Within the final month, the holding purchased over 19.5 million extra Philips shares for roughly €481 million. Right here on the Lab, we lately commented on Koninklijke Philips with an replace known as Main Overhang Eliminated. Philips agreed to pay $1.1 billion to settle the Respironics litigation in the US. Reporting our evaluation, we beforehand estimated a possible $3 billion lawsuit based mostly on 100,000 complaints with a minimal previous expense of $30k every. Our evaluation of previous pharma lawsuits backed this. For that reason, our crew determined to extend Philips’ monetary EPS and raised our goal value to €26 per share.

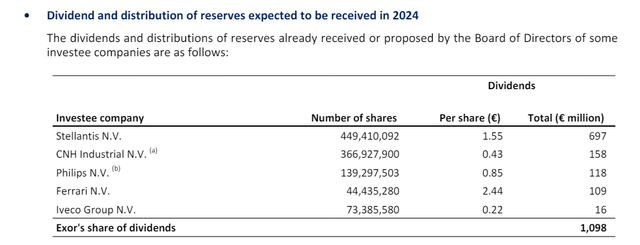

(Supportive shareholders’ remuneration linked to Exor portfolio outcomes). Exor owns 14.87% of Stellantis’ excellent shares. The Automotive group lately launched an Investor Day with reassuring phrases for 2024. Stellantis expects an adjusted working revenue margin within the 10%-11% space in H1 2024, with additional upside in H2 because of incremental price discount. That is additionally supported by platforms & provide chain price focus to safeguard double-digit margins. Associated to capital allocation priorities, Stellantis communicated its choice to purpose for greater shareholders’ remuneration with a payout coverage within the excessive finish of the 25%-30% vary. On the present share value, Stellantis CEO targets a plus 10% complete remuneration mixed with dividends & share buybacks. These statements make our crew assured that the lion’s share of annual free money stream technology will likely be returned to shareholders. In our estimates, we forecast a DPS change from €1.55 to €1.6, transferring Exor dividend to €720 million.

Final week, the automotive jewel in Exor galaxy (Ferrari) determined to open a long-awaited e-factory, the place it plans the manufacturing of its first electrical automotive, which will likely be offered in H2 2025. Ferrari’s CEO reiterated that the brand new facility goals to extend deliveries by greater than 14,000 items yearly. This new e-factory gives Ferrari with flexibility, greater automatization, and an upside from its personalization functionality. This additionally means the next margin over the medium-term and possibly greater DPS. For that reason, we improve our DPS to €2.72 per share for the next yr. This represents a rise of 11% with an Exor distribution of €120 million.

Concerning Ivece, publish Q1 outcomes, the group lively within the manufacturing of economic autos achieved an adjusted internet revenue of €153 million, with the entire industrial enterprise items – Truck, Bus, Protection, and Powertrain – that signed margin enhancements. Contemplating CNH Industrial and Phillips DPS, right here on the Lab, we consider that Exor would possibly attain €1.2 billion in distribution for 2025. Subsequently, it’s not stunning that Exor re-started on 15 April 2024 with a primary tranche of buyback of as much as €125 million, anticipated to be accomplished by September 2024.

Exor dividend contribution

Supply: Exor press launch

(Exor Ventures Upside). Even when we’re not pricing the Ventures arm into Exor’s market cap, this crew goals to spend money on early-stage corporations with a everlasting capital view. The corporate secured two of essentially the most enticing VC offers final month. Intimately, Exor Ventures participated in a $10 million spherical in Viaduct. This automotive startup has developed AI-based expertise able to figuring out, fixing, and even predicting doable product failures. Additionally, Stellantis Ventures determined to step in. The second funding was within the French startup Zeliq, which nonetheless makes use of AI however provides options to simplify product gross sales. On this case, Exor Ventures led the €9.2 million spherical, during which the VC Resonance fund additionally participated.

Valuation

Publish outcomes, the corporate’s NAV reached €162.4 per share, whereas Exor’s present inventory value is €98 per share. Subsequently, we stay consumers of Exor with a goal value of €113 per share. The present 40% NAV low cost is near record-high ranges and unjustified in our view. Right here on the Lab, we apply a 30% low cost to NAV (unchanged), aligned with Exor’s long-term historic common, and ensure our purchase score.

Exor Ranking Replace

Dangers

Draw back dangers embrace operational efficiency at essential holdings resembling Stellantis and Ferrari. As well as, Exor’s valuation relies on the NAV low cost. A part of Exor’s portfolio just isn’t listed; due to this fact, it’s onerous to justify an accurate analysis. That mentioned, Exor may be very a lot depending on the automotive development. This contains 1) greater competitors, 2) change in client tastes, 3) new product growth dangers, and 4) labor inflation.

Conclusion

Our funding thesis focuses on unjustified holding reductions and supportive shareholders’ remuneration. We additionally see help from Ferrari and Stellantis companies and positively view Exor’s choice to extend the fairness stake in Philips. For that reason, our goal value and purchase score is confirmed.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

[ad_2]

Source link

Q3 2024 Earnings Call Transcript")

")

{kind=link}