[ad_1]

From our earlier research, we all know that calendar time spreads have optimistic vega.

Vega is among the choices Greeks use to tell us of how the commerce will revenue if implied volatility adjustments.

Contents

When a commerce has optimistic vega — we name this a protracted vega commerce — it implies that it ought to revenue if implied volatility goes up, supplied that volatility was the one factor that modified.

We are saying that it “ought to” as a result of that is considerably theoretical.

In actuality, it could or might not, relying on many components.

The revenue is affected by the opposite Greeks, primarily Delta, which causes the revenue and loss (P&L) to alter as the worth of the underlying strikes.

One other Greek is Theta.

For calendars, theta is optimistic, which means {that a} portion of the calendar worth will enhance each day (together with non-trading days).

One other issue that impacts the worth of the calendar is how the implied volatility of the near-term possibility adjustments in relation to the far-term possibility.

This subject entails the quantity of skew and contango, which we won’t talk about at this time.

Regardless, some choices merchants want to configure the quantity of vega of their calendars, which is the subject of at this time’s dialogue.

The vega within the calendar is a perform of the distinction in vega between the lengthy and quick choices.

If the dealer desires to lower the quantity of vega within the calendar, essentially the most available methodology is to lower the time between the close to and the far-term possibility.

When the 2 expirations are shut to one another, their volatility variations often might be much less.

Therefore, vega is much less.

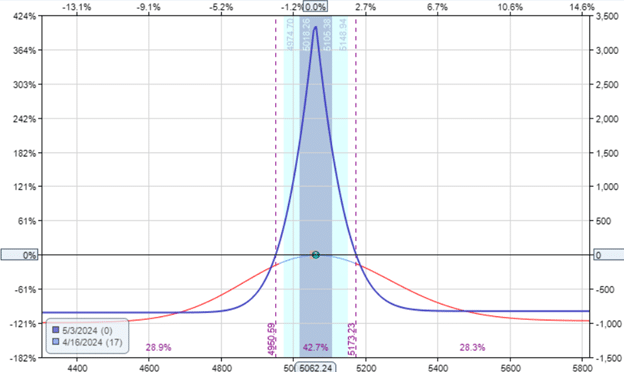

For instance, here’s a calendar with one week between the near-term quick possibility and the far-term lengthy possibility.

Date: April 16, 2024

Worth: SPX @ 5062

Promote one contract Could third SPX 5060 put @ $69.25Buy one contract Could tenth SPX 5060 put @ $77.50

Debit: -$825

Delta: 0.15Theta: 44.91Vega: 81.91Vega/Theta: 1.8

It has a vega of 82.

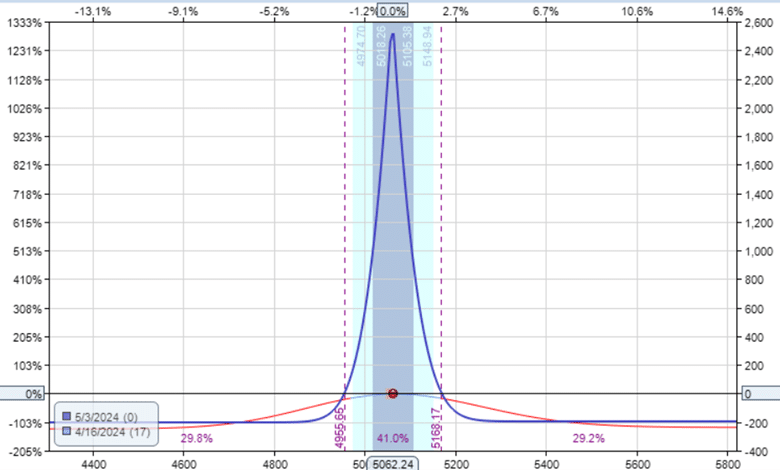

If we preserve the near-term possibility the identical however transfer the expiration of the far-term possibility nearer to lower the time hole between the expiration of the 2 choices, we might have the next calendar:

Date: April 16, 2024

Worth: SPX @ 5062

Promote one contract Could third SPX 5060 put @ $69.25Buy one contract Could 6 SPX 5060 put @ $71.20

Debit: -$195

10X Your Choices Buying and selling

Delta: 0.01Theta: 27.57Vega: 36.85Vega/Theta: 1.3

The vega has now decreased to 36.85.

However we’ve got additionally misplaced theta.

That is true as a result of this calendar is smaller and narrower (as you may see by evaluating the width of the expiration break-even factors).

Nonetheless, the loss in theta just isn’t proportional to the loss in vega (as could be famous by the distinction within the Vega/Theta ratio).

In different phrases, we will have two such slim calendars like this:

Date: April 16, 2024

Worth: SPX @ 5062

Promote two contract Could third SPX 5060 put @ $69.25Buy two contract Could 6 SPX 5060 put @ $71.20

Debit: -$390

And the Greeks could be cumulative.

Delta: 0.02Theta: 55.13Vega: 73.70Vega/Theta: 1.3

We’ve got simply as a lot and much more theta than the vast calendar.

And but, our cumulative vega continues to be lower than our vast calendar.

Decreasing the DTE

One other strategy to lower the vega/theta ratio is to cut back the days to expiration.

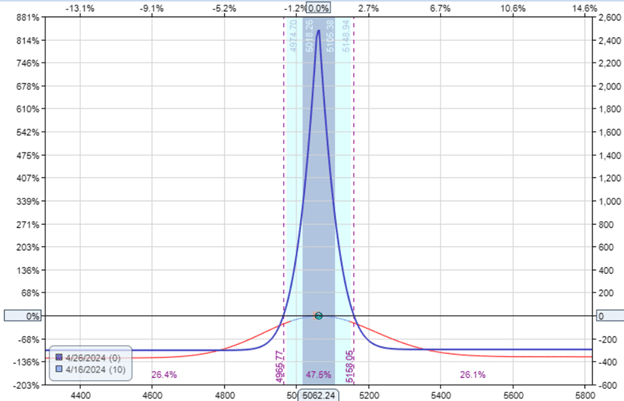

Right here, we’ve got a calendar with solely ten days until expiration for the quick possibility.

The lengthy possibility continues to be three days additional than the quick possibility.

Date: April 16, 2024

Worth: SPX @ 5062

Promote one contract April 26 SPX 5060 put @ $55.60Buy one contract April 29 SPX 5060 put @ $58.55

Debit: -$295

The Greeks, for one contract, are:

Delta: 0.02Theta: 55.15Vega: 46.81

These Greeks allow us to calculate the Vega/Theta ratio to be 0.84, decrease than any of the instance calendars proven to this point.

By decreasing the variety of days to expiration, we’ve got decreased vega in relation to theta.

Suppose you consider vega because the volatility danger in a calendar.

And consider theta because the incoming era engine of the calendar.

Then, a decrease vega/theta ratio means a decrease risk-to-reward ratio, which is one other method of stating a greater reward-to-risk ratio.

We’re saying that by reducing the time hole between expirations and by reducing the times to expiration, we’re rising the reward-to-risk ratio of the calendar.

This calendar is even smaller and narrower:

Studying off the graph, we see the reward-to-risk is about $2500 / $300 = 8.3.

The dealer may wish to enhance the variety of contracts to realize the place dimension that they need.

Nonetheless, the Vega/Theta ratio won’t change because the variety of contracts will increase.

Calendars become profitable from the theta.

The vega represents volatility danger.

Merchants who wish to lower their vega danger on their calendars with out compromising on theta will wish to lower the vega in relation to the theta.

In different phrases, they need calendars with decrease vega/theta ratios.

The vega/theta ratio could be diminished by reducing the time distinction between the expirations of the 2 choices.

The form of the calendar expiration graph will look extra slim.

The vega/theta ratio may also be diminished by reducing the variety of days until expiration (assuming we preserve the time distinction between the 2 choices the identical).

Tall skinny calendars might have a decrease vega/theta ratio, which is sweet.

Nonetheless, in addition they have a slim vary of profitability, which isn’t so good.

We hope you loved this text on controlling the vega of calendar spreads.

When you have any questions, please ship an e mail or depart a remark beneath.

Commerce secure!

Disclaimer: The data above is for academic functions solely and shouldn’t be handled as funding recommendation. The technique introduced wouldn’t be appropriate for buyers who are usually not aware of trade traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.

[ad_2]

Source link

, Boeing (NYSE:BA)")

{kind=link}