[ad_1]

Over the previous couple of years traders have not been in a position to purchase semiconductor shares quick sufficient. An enormous purpose for it is because subtle chips often known as graphics processing items (GPUs) are one of many core energy sources of synthetic intelligence (AI) purposes reminiscent of machine studying and even autonomous driving.

Because the AI narrative continues to push the markets increased, chip shares will possible stay in excessive demand. Because it stands at the moment, Nvidia is extensively thought of to be the market chief amongst AI-powered chip firms. Nonetheless, Nvidia simply instructed traders that the corporate’s new Blackwell sequence GPUs are going to be delayed as a consequence of a design flaw.

Whereas I am no supporter of schadenfreude, I see this setback at Nvidia as a once-in-a-lifetime second for the corporate’s greatest competitor, Superior Micro Gadgets (NASDAQ: AMD). Let’s look at the total scenario at hand and assess how AMD may benefit from Nvidia’s hiccup.

A story of two chip firms

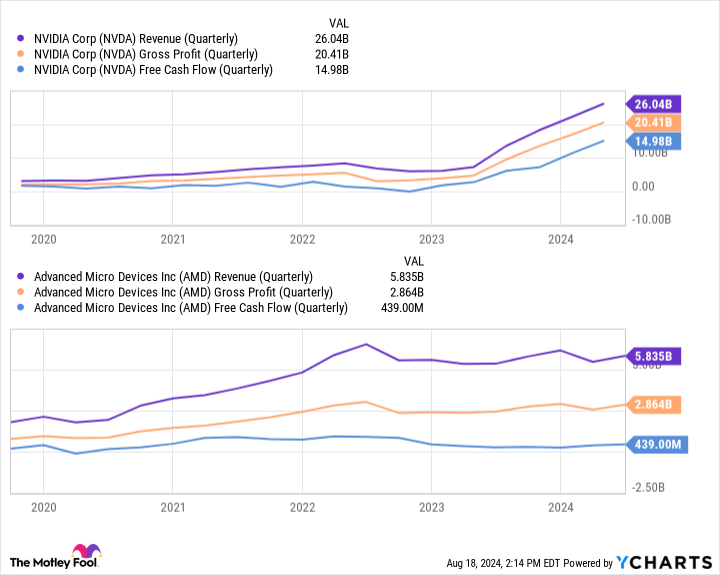

The charts beneath illustrate quite a lot of essential monetary metrics for Nvidia and AMD.

On one aspect of the equation, Nvidia’s gross sales and income are persistently hovering — resulting in an more and more steeper slope among the many coloured strains depicted beneath. But on the opposite aspect, Nvidia’s chief rival is demonstrating noticeable inconsistencies in its operation.

The dynamics illustrated above clearly point out that chip patrons not solely favor Nvidia, however are additionally prepared to pay high greenback. Though Nvidia has remained the supreme semiconductor firm because the inception of the AI revolution, AMD has an unimaginable alternative to leapfrog Nvidia proper now.

Why this could be AMD’s defining second

Wall Road analysts estimate that Nvidia has practically 80% of the AI-powered chip market. Whereas AMD has finished what it might probably to compete with Nvidia’s beautiful tempo of innovation, I believe the corporate has largely tried to distract traders from Nvidia’s overwhelming lead by way of a sequence of questionable acquisitions.

To me, AMD’s time is near working out and it might probably’t afford to depend on acquisitions as a supply of product growth and inorganic development. One silver lining for AMD proper now could be that the corporate’s MI300X accelerator GPU is the quickest product to achieve $1 billion in gross sales over the corporate’s historical past.

Clearly, there may be lots of demand for AMD’s GPUs, however it’s simply not even in the identical breadth as Nvidia’s demand. Now with Blackwell shipments delayed till presumably someday subsequent 12 months, AMD has an opportunity to grab the second.

Story continues

It is essential to remain grounded

Whereas the Blackwell delays are on no account excellent news, traders have to be actual right here. I surmise some firms will go for different options to Blackwell within the interim, however I do not assume Nvidia can have a tough time promoting these chips as soon as it lastly repairs its design flaw.

So despite the fact that AMD possible is not going to all of the sudden seize an awesome quantity of market share and outright dethrone Nvidia, I believe the corporate has an opportunity to boost its profile by disrupting Nvidia’s momentum.

For now, it will be nearly unattainable for traders to know if AMD is penetrating the market whereas Nvidia focuses on righting the Blackwell ship. I believe some prudent actions might be to observe press releases amongst main AI builders reminiscent of Microsoft, Amazon, Alphabet, or Oracle and see if any of them are hanging new partnerships with AMD or shopping for extra MI300X chips.

Though I do not personal AMD inventory in the mean time, I’m intrigued by the present dynamics of the chip market and see the corporate as each a hedge to Nvidia and much like a long-term name possibility on the AI market extra broadly.

Buyers with a better tolerance for danger, nonetheless, might think about shopping for AMD now. Given the corporate is taking part in second fiddle to Nvidia, it is exhausting to think about a state of affairs the place AMD falls behind within the midst of this Blackwell scenario.

One other technique might be to attend a few months till AMD publishes its subsequent earnings report and see if the corporate generated irregular development in comparison with prior durations. Buyers must also hearken to administration’s commentary relating to the supply of latest enterprise.

In both case, I’m bullish that AMD will benefit from Nvidia’s stumble and maybe ignite the catalyst wanted for longer-term sustained development as the 2 firms proceed going face to face within the chip realm.

Must you make investments $1,000 in Superior Micro Gadgets proper now?

Before you purchase inventory in Superior Micro Gadgets, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the 10 greatest shares for traders to purchase now… and Superior Micro Gadgets wasn’t considered one of them. The ten shares that made the lower may produce monster returns within the coming years.

Contemplate when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $758,227!*

Inventory Advisor supplies traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of August 22, 2024

Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Alphabet, Amazon, Microsoft, and Nvidia. The Motley Idiot has positions in and recommends Superior Micro Gadgets, Alphabet, Amazon, Microsoft, Nvidia, and Oracle. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

AMD’s Leapfrog Second Has Arrived. This is Why Now Might Be a As soon as-in-a-Lifetime Alternative to Purchase the Inventory. was initially revealed by The Motley Idiot

[ad_2]

Source link

Q3 2024 Earnings Call Transcript")

")