[ad_1]

Artwork Wager

Antero Midstream (NYSE:NYSE:AM) is a midstream power operator with a market cap of simply over $7 billion. AM portfolio property are comprised of gathering pipelines, compression services, pursuits in processing and fractionation vegetation, and water dealing with programs. AM can be lively in establishing joint ventures to develop enter into bigger tasks with out assuming full threat. Right here essentially the most notable JV of AM is fashioned along with MPLX LP (NYSE:MPLX), the place the underlying operations are round creating and working massive scale processing and fractionation property.

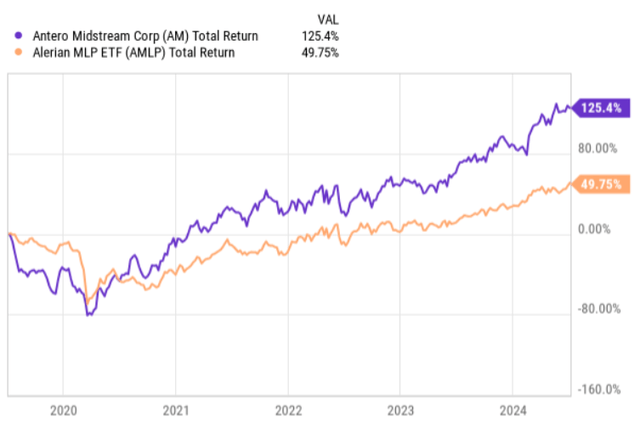

If we have a look at the historic five-year complete return efficiency and evaluate it with the general midstream section, we’ll clearly see how persistently AM has generated alpha over the related index. Within the chart beneath it’s evident that actually ranging from early 2020, AM has assumed a robust and upward-sloping return trajectory.

Ycharts

Such a notable hole within the registered returns might elevate a query on whether or not AM’s valuations have gone too removed from the underlying worth. The truth is, comparatively just lately UBS lower its score on AM from purchase to carry referring to the truth that the chance and reward profile has reached an equilibrium.

Furthermore, the present dividend yield supplied by AM just isn’t that attractive in comparison with what we are able to discover within the midstream area. At the moment, AM yields solely 6.1%, which is circa 120 foundation factors beneath the yield of Alerian MLP ETF (NYSEARCA:AMLP) index.

Let’s now assess the underlying fundamentals of AM to find out whether or not it is sensible to go lengthy right here.

Thesis

At its core, AM is a fairly comparable enterprise to its friends equivalent to Enterprise Merchandise Companions (NYSE:EPD), Enbridge (ENB), Vitality Switch (NYSE:ET), MPLX, and many others. The enterprise mannequin is constructed on sturdy pure gasoline infrastructure property, which get pleasure from virtually a everlasting demand profile with the one exceptions within the money era stemming from potential operational failures. Apart from that, AM is ready to generate constant and periodically rising money flows which might be backed by sound contracts.

The one points that materially distinguish AM from its friends are the next two:

100% of AM’s money era is underpinned by fixed-fee contracts, thus mitigating the commodity threat issue. Versus most of its friends, AM is sort of totally centered on pure gasoline section, which is inherently extra favorable from the valuations perspective (i.e., introduces a better predictability within the enterprise).

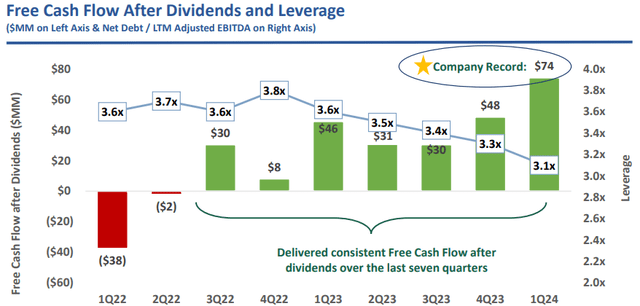

Furthermore, as for many of midstream firms, the latest monetary efficiency for AM has been very sturdy. For instance, Q1, 2024 was a document quarter for AM, with the natural progress touchdown at a 4% and 6% in gathering and processing volumes, respectively, in comparison with final 12 months. When it comes to the EBITDA era, AM registered a double-digit EBITDA progress, whereas reaching a double-digit declines within the CapEx spend. On account of these dynamics, AM landed document free money movement ranges of $182 million and $74 million if we modify for the dividend funds.

Right here the chart beneath captures properly how AM has been sticking to a free money movement centered technique since Q3, 2022, when it began to persistently register surplus outcomes (after accounting for dividend distributions).

Antero Midstream Investor Presentation

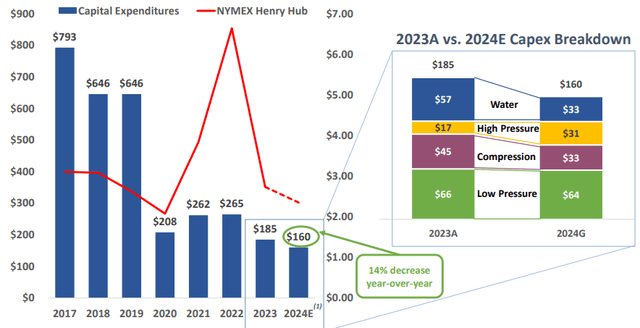

A part of that is clearly pushed by the earlier CapEx applications coming on-line and AM’s success in natural progress, however one of many key causes is clearly the diminished CapEx spend.

Antero Midstream Investor Presentation

What we are able to discover on this CapEx associated chart is that AM stays fairly dedicated on reducing the natural CapEx even additional, which ought to per definition depart extra liquidity at AM’s books to both de-risk the steadiness sheet or conduct buybacks.

The commentary within the latest earnings name by Brendan Krueger – CFO of Antero Midstream – supplied an fascinating coloration on this regard:

Sure. Thanks for the query. That is Brendan. I feel as we have talked about on previous calls as effectively, I imply, we have a look at all the things by way of return and on general capital. So, as we method this 3x leverage goal, as we talked about, second half of this 12 months, we’ll look to — it will likely be positioned us effectively to purchase again shares or pay down additional debt or execute for the bolt-on acquisitions. We have got the $500 million program on the market, as you talked about, and we do see attractiveness in our shares nonetheless at present. So, as we sit right here at present, share buybacks would proceed to make numerous sense, however we’ll actually consider that as we as we hit that 3x goal, hopefully, within the second half of this 12 months.

Aside from the natural CapEx spend, there may be additionally an M&A element that may briefly drive the excess money era ranges of AM decrease. For example, Might this 12 months, AM introduced that it has ventured right into a bolt-on acquisition of property in Marcellus Shale at a ticket measurement of $70 million.

Whereas this may introduce some problem for AM to maintain de-risking the steadiness sheet and / or get pleasure from rising surplus money movement ranges, now we have to remember that basically the M&A transactions are accretive and in AM’s case usually of a small scale. Even wanting on the remark above by Brendan Krueger, we are able to see that the administration stays dedicated on bringing the online debt to EBITDA at 3x.

Talking of the steadiness sheet, presently, AM carries a web debt to EBITDA of three.1x, which isn’t the bottom stage within the sector, however nonetheless an indicative of a sound capital construction. On prime of this, AM has no debt maturities in 2024 and 2025, and the one, which comes due in 2026 is expounded to the credit score revolver.

The underside line

All in all, Antero Midstream enterprise is powerful and underpinned by sound financials each from the money era and capital construction perspective. The truth that all the contracts are primarily based on fixed-fee and that the operations are virtually totally primarily based in pure gasoline segments ought to warrant some premium. Whereas the steadiness sheet just isn’t the strongest within the sector, the distant debt maturity profile together with a concentrate on de-leveraging render AM fascinating additionally from this angle.

Nonetheless, with all of this being mentioned, I’m nonetheless hesitant to go lengthy AM. The reason being easy – on the whole, I agree with UBS’s view that the upside potential is basically exhausted. The latest run-up within the share value has pushed the valuations increased accordingly (EV/EBITDA of 12x, which is on the excessive finish in midstream area), making the dividend yield of ~ 6% comparatively unattractive.

For me, there are higher midstream alternate options on the market, the place the dividend yields are increased, steadiness sheets stronger and progress prospects fairly just like what Antero Midstream has outlined. Beneath are simply three examples, the place I’ve issued purchase thesis:

MPLX LP yielding 8% (see article right here). Vitality Switch yielding 7.8% (see article right here) Enterprise Merchandise Companions yielding 7.1% (see article right here)

[ad_2]

Source link

")

")

")

Q3 2024 Earnings Call Transcript")

{kind=link}